In this article, we’ll demonstrate how to create a machine learning model for predicting buy and sell signals in the ETH/USD market using a Random Forest algorithm. We’ll walk through the entire process, from importing libraries and data, to preprocessing, feature engineering, model training, hyperparameter tuning, and evaluation. Finally, we’ll test our model on live data and backtest the predictions using vectorbt to gauge its potential profitability.

By following this tutorial, you’ll gain a deeper understanding of the application of machine learning techniques in the field of cryptocurrency trading and learn how to leverage the power of Random Forest for predicting market movements. Whether you’re an experienced trader or a machine learning enthusiast, this article will provide valuable insights and practical guidance to help you build your own trading strategies.

Importing Libraries and Data

First, let’s import the necessary libraries and set up the API connection.

import pandas as pd

import pandas_ta as ta

import numpy as np

import vectorbt as vbt

import yfinance as yf

from datetime import datetime

import matplotlib.pyplot as plt

import pydot

import vectorbt as vbt

import ccxtinitial ccxt and symbol

exchange = ccxt.binance()

symbol = 'ETH/USDT'

timeframe = '4h'Fetching Historical Data

We’ll fetch historical OHLCV data from the Binance exchange starting from 2015.

# get OHLCV 4h. focus on bear market 2018 , 2022 i want to create some stretegies to protect my wealth when bear market coming

from_ts = exchange.parse8601('2015-11-01 00:00:00')

ohlcv_list = []

ohlcv = exchange.fetch_ohlcv(symbol, timeframe, since=from_ts, limit=1000)

ohlcv_list.append(ohlcv)

while True:

from_ts = ohlcv[-1][0]

new_ohlcv = exchange.fetch_ohlcv(symbol, timeframe, since=from_ts, limit=1000)

ohlcv.extend(new_ohlcv)

if len(new_ohlcv)!=1000:

breakohlcv_list

[[[1502942400000, 301.13, 307.96, 298.0, 307.96, 1561.95305],

[1502956800000, 307.95, 312.0, 307.0, 308.95, 1177.71088],

[1502971200000, 308.95, 310.51, 303.56, 307.06, 1882.05267],

...

[1517284800000, 1137.96, 1178.92, 1130.08, 1174.96, 14730.37261],

[1517299200000, 1174.05, 1186.85, 1156.0, 1169.89, 12918.61121],

[1517313600000, 1167.16, 1175.0, 1101.0, 1112.09, 26607.01368],

[1517328000000, 1112.5, 1133.01, 1051.0, 1112.11, 51675.82377],

...]]Next, we’ll create a DataFrame with the fetched data.

ohlcv_list = [[item[0], item[1], item[2], item[3], item[4], item[5]] for item in ohlcv_list[0]]

# create a DataFrame from the list OHLCV from 2021-11-01 to 2023-03-16

df = pd.DataFrame(ohlcv_list, columns=['timestamp', 'open', 'high', 'low', 'close', 'volume'])

df

we will see dataframe like this

| timestamp | open | high | low | close | volume | |

|---|---|---|---|---|---|---|

| 0 | 1502942400000 | 301.13 | 307.96 | 298.00 | 307.96 | 1561.95305 |

| 1 | 1502956800000 | 307.95 | 312.00 | 307.00 | 308.95 | 1177.71088 |

| 2 | 1502971200000 | 308.95 | 310.51 | 303.56 | 307.06 | 1882.05267 |

| 3 | 1502985600000 | 307.74 | 312.18 | 298.21 | 301.60 | 1208.05192 |

| 4 | 1503000000000 | 301.60 | 310.85 | 299.01 | 302.00 | 1200.94182 |

| … | … | … | … | … | … | … |

| 12220 | 1678968000000 | 1660.37 | 1666.73 | 1635.96 | 1663.06 | 129192.79690 |

| 12221 | 1678982400000 | 1663.06 | 1691.42 | 1652.88 | 1679.64 | 113369.52090 |

| 12222 | 1678996800000 | 1679.64 | 1681.78 | 1652.53 | 1673.73 | 76922.01860 |

| 12223 | 1679011200000 | 1673.73 | 1725.00 | 1662.65 | 1708.62 | 166034.43070 |

| 12224 | 1679025600000 | 1708.62 | 1730.99 | 1696.37 | 1715.56 | 103495.68750 |

12225 rows × 6 columns

Preparing the Data

Now, we’ll prepare the data by adding timestamps and various technical indicators.

Add timestamp and set index

df_action=df.copy()

df_action['timestamp'] = pd.to_datetime(df['timestamp'], unit='ms')

df_action.reset_index(inplace=True)

df_action.set_index(df_action['timestamp'],inplace=True)

df_action| index | timestamp | open | high | low | close | volume | |

|---|---|---|---|---|---|---|---|

| timestamp | |||||||

| 2017-08-17 04:00:00 | 0 | 2017-08-17 04:00:00 | 301.13 | 307.96 | 298.00 | 307.96 | 1561.95305 |

| 2017-08-17 08:00:00 | 1 | 2017-08-17 08:00:00 | 307.95 | 312.00 | 307.00 | 308.95 | 1177.71088 |

| 2017-08-17 12:00:00 | 2 | 2017-08-17 12:00:00 | 308.95 | 310.51 | 303.56 | 307.06 | 1882.05267 |

| 2017-08-17 16:00:00 | 3 | 2017-08-17 16:00:00 | 307.74 | 312.18 | 298.21 | 301.60 | 1208.05192 |

| 2017-08-17 20:00:00 | 4 | 2017-08-17 20:00:00 | 301.60 | 310.85 | 299.01 | 302.00 | 1200.94182 |

| … | … | … | … | … | … | … | … |

| 2023-03-16 12:00:00 | 12220 | 2023-03-16 12:00:00 | 1660.37 | 1666.73 | 1635.96 | 1663.06 | 129192.79690 |

| 2023-03-16 16:00:00 | 12221 | 2023-03-16 16:00:00 | 1663.06 | 1691.42 | 1652.88 | 1679.64 | 113369.52090 |

| 2023-03-16 20:00:00 | 12222 | 2023-03-16 20:00:00 | 1679.64 | 1681.78 | 1652.53 | 1673.73 | 76922.01860 |

| 2023-03-17 00:00:00 | 12223 | 2023-03-17 00:00:00 | 1673.73 | 1725.00 | 1662.65 | 1708.62 | 166034.43070 |

| 2023-03-17 04:00:00 | 12224 | 2023-03-17 04:00:00 | 1708.62 | 1730.99 | 1696.37 | 1715.56 | 103495.68750 |

12225 rows × 7 columns

add MACD indicator

df_action.ta.macd(append=True)

df_action| index | timestamp | open | high | low | close | volume | MACD_12_26_9 | MACDh_12_26_9 | MACDs_12_26_9 | |

|---|---|---|---|---|---|---|---|---|---|---|

| timestamp | ||||||||||

| 2017-08-17 04:00:00 | 0 | 2017-08-17 04:00:00 | 301.13 | 307.96 | 298.00 | 307.96 | 1561.95305 | NaN | NaN | NaN |

| 2017-08-17 08:00:00 | 1 | 2017-08-17 08:00:00 | 307.95 | 312.00 | 307.00 | 308.95 | 1177.71088 | NaN | NaN | NaN |

| 2017-08-17 12:00:00 | 2 | 2017-08-17 12:00:00 | 308.95 | 310.51 | 303.56 | 307.06 | 1882.05267 | NaN | NaN | NaN |

| 2017-08-17 16:00:00 | 3 | 2017-08-17 16:00:00 | 307.74 | 312.18 | 298.21 | 301.60 | 1208.05192 | NaN | NaN | NaN |

| 2017-08-17 20:00:00 | 4 | 2017-08-17 20:00:00 | 301.60 | 310.85 | 299.01 | 302.00 | 1200.94182 | NaN | NaN | NaN |

| … | … | … | … | … | … | … | … | … | … | … |

| 2023-03-16 12:00:00 | 12220 | 2023-03-16 12:00:00 | 1660.37 | 1666.73 | 1635.96 | 1663.06 | 129192.79690 | 26.487664 | -9.729147 | 36.216810 |

| 2023-03-16 16:00:00 | 12221 | 2023-03-16 16:00:00 | 1663.06 | 1691.42 | 1652.88 | 1679.64 | 113369.52090 | 26.074843 | -8.113574 | 34.188417 |

| 2023-03-16 20:00:00 | 12222 | 2023-03-16 20:00:00 | 1679.64 | 1681.78 | 1652.53 | 1673.73 | 76922.01860 | 24.982806 | -7.364488 | 32.347295 |

| 2023-03-17 00:00:00 | 12223 | 2023-03-17 00:00:00 | 1673.73 | 1725.00 | 1662.65 | 1708.62 | 166034.43070 | 26.625765 | -4.577224 | 31.202989 |

| 2023-03-17 04:00:00 | 12224 | 2023-03-17 04:00:00 | 1708.62 | 1730.99 | 1696.37 | 1715.56 | 103495.68750 | 28.163175 | -2.431851 | 30.595026 |

12225 rows × 10 columns

create MACD trend when MACD line > MACD signals line

df_action['macd_trend']= df_action.MACD_12_26_9 > df_action.MACDs_12_26_9Add RSI indicator

df_action.ta.rsi(append=True)

timestamp

2017-08-17 04:00:00 NaN

2017-08-17 08:00:00 NaN

2017-08-17 12:00:00 NaN

2017-08-17 16:00:00 NaN

2017-08-17 20:00:00 NaN

...

2023-03-16 12:00:00 56.716544

2023-03-16 16:00:00 59.590967

2023-03-16 20:00:00 58.109595

2023-03-17 00:00:00 63.826631

2023-03-17 04:00:00 64.854113

Name: RSI_14, Length: 12225, dtype: float64Add RSI labels to dataframe

RSI < 50 = -1 and other is 1

df_action.loc[df_action['RSI_14']>75,'overbought']= 1

df_action.loc[df_action['RSI_14']<30,'oversold']= 1

df_action.loc[df_action['RSI_14']>50,'RSI_trend']= 1

df_action.loc[df_action['RSI_14']<50,'RSI_trend']=-1preview dataframe

df_action| index | timestamp | open | high | low | close | volume | MACD_12_26_9 | MACDh_12_26_9 | MACDs_12_26_9 | macd_trend | RSI_14 | overbought | oversold | RSI_trend | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| timestamp | |||||||||||||||

| 2017-08-17 04:00:00 | 0 | 2017-08-17 04:00:00 | 301.13 | 307.96 | 298.00 | 307.96 | 1561.95305 | NaN | NaN | NaN | False | NaN | NaN | NaN | NaN |

| 2017-08-17 08:00:00 | 1 | 2017-08-17 08:00:00 | 307.95 | 312.00 | 307.00 | 308.95 | 1177.71088 | NaN | NaN | NaN | False | NaN | NaN | NaN | NaN |

| 2017-08-17 12:00:00 | 2 | 2017-08-17 12:00:00 | 308.95 | 310.51 | 303.56 | 307.06 | 1882.05267 | NaN | NaN | NaN | False | NaN | NaN | NaN | NaN |

| 2017-08-17 16:00:00 | 3 | 2017-08-17 16:00:00 | 307.74 | 312.18 | 298.21 | 301.60 | 1208.05192 | NaN | NaN | NaN | False | NaN | NaN | NaN | NaN |

| 2017-08-17 20:00:00 | 4 | 2017-08-17 20:00:00 | 301.60 | 310.85 | 299.01 | 302.00 | 1200.94182 | NaN | NaN | NaN | False | NaN | NaN | NaN | NaN |

| … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … |

| 2023-03-16 12:00:00 | 12220 | 2023-03-16 12:00:00 | 1660.37 | 1666.73 | 1635.96 | 1663.06 | 129192.79690 | 26.487664 | -9.729147 | 36.216810 | False | 56.716544 | NaN | NaN | 1.0 |

| 2023-03-16 16:00:00 | 12221 | 2023-03-16 16:00:00 | 1663.06 | 1691.42 | 1652.88 | 1679.64 | 113369.52090 | 26.074843 | -8.113574 | 34.188417 | False | 59.590967 | NaN | NaN | 1.0 |

| 2023-03-16 20:00:00 | 12222 | 2023-03-16 20:00:00 | 1679.64 | 1681.78 | 1652.53 | 1673.73 | 76922.01860 | 24.982806 | -7.364488 | 32.347295 | False | 58.109595 | NaN | NaN | 1.0 |

| 2023-03-17 00:00:00 | 12223 | 2023-03-17 00:00:00 | 1673.73 | 1725.00 | 1662.65 | 1708.62 | 166034.43070 | 26.625765 | -4.577224 | 31.202989 | False | 63.826631 | NaN | NaN | 1.0 |

| 2023-03-17 04:00:00 | 12224 | 2023-03-17 04:00:00 | 1708.62 | 1730.99 | 1696.37 | 1715.56 | 103495.68750 | 28.163175 | -2.431851 | 30.595026 | False | 64.854113 | NaN | NaN | 1.0 |

12225 rows × 15 columns

Creating the Machine Learning Model

First, we’ll create signals based on the MACD trend. and check macd trend is shift and add iloc 2 cause want to shift fist signal shift macd at starts have noise to avoid that should shift

Next, we’ll create the Random Forest model, preprocess the data, and split it into training and testing sets.

signaled=df_action[df_action['macd_trend'].shift(1)!= df_action['macd_trend']].iloc[2:]

signaled| index | timestamp | open | high | low | close | volume | MACD_12_26_9 | MACDh_12_26_9 | MACDs_12_26_9 | macd_trend | RSI_14 | overbought | oversold | RSI_trend | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| timestamp | |||||||||||||||

| 2017-08-26 00:00:00 | 53 | 2017-08-26 00:00:00 | 327.24 | 332.27 | 323.41 | 323.46 | 569.57801 | 5.218425 | -0.144303 | 5.362728 | False | 53.515087 | NaN | NaN | 1.0 |

| 2017-08-27 16:00:00 | 63 | 2017-08-27 16:00:00 | 335.04 | 341.47 | 332.97 | 339.64 | 795.13177 | 5.146901 | 0.285160 | 4.861741 | True | 68.589301 | NaN | NaN | 1.0 |

| 2017-08-31 16:00:00 | 87 | 2017-08-31 16:00:00 | 384.38 | 387.39 | 383.13 | 384.45 | 878.88372 | 12.619776 | -0.009218 | 12.628994 | False | 73.658395 | NaN | NaN | 1.0 |

| 2017-09-05 16:00:00 | 117 | 2017-09-05 16:00:00 | 290.07 | 321.52 | 285.94 | 318.26 | 677.80125 | -17.420385 | 0.985630 | -18.406015 | True | 48.964468 | NaN | NaN | -1.0 |

| 2017-09-08 12:00:00 | 134 | 2017-09-08 12:00:00 | 330.10 | 331.57 | 272.00 | 294.05 | 2343.12862 | -1.422169 | -0.756305 | -0.665864 | False | 36.802842 | NaN | NaN | -1.0 |

| … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … |

| 2023-03-03 00:00:00 | 12139 | 2023-03-03 00:00:00 | 1647.86 | 1649.25 | 1544.39 | 1565.44 | 317798.34160 | -2.231587 | -5.079240 | 2.847653 | False | 34.504987 | NaN | NaN | -1.0 |

| 2023-03-05 08:00:00 | 12153 | 2023-03-05 08:00:00 | 1568.61 | 1573.07 | 1564.03 | 1568.50 | 32527.56420 | -16.383615 | 0.212968 | -16.596583 | True | 38.888106 | NaN | NaN | -1.0 |

| 2023-03-08 20:00:00 | 12174 | 2023-03-08 20:00:00 | 1552.72 | 1561.29 | 1523.61 | 1532.38 | 128310.87040 | -9.161005 | -0.786086 | -8.374919 | False | 32.613518 | NaN | NaN | -1.0 |

| 2023-03-11 16:00:00 | 12191 | 2023-03-11 16:00:00 | 1428.00 | 1457.04 | 1422.32 | 1449.22 | 180365.58850 | -32.769032 | 1.859142 | -34.628174 | True | 42.608536 | NaN | NaN | -1.0 |

| 2023-03-15 12:00:00 | 12214 | 2023-03-15 12:00:00 | 1679.91 | 1698.29 | 1625.56 | 1634.04 | 313571.19570 | 46.865502 | -3.715414 | 50.580916 | False | 52.346900 | NaN | NaN | 1.0 |

921 rows × 15 columns

create return

signaled['return']=signaled['close'].pct_change().shift(-1)

signaled| index | timestamp | open | high | low | close | volume | MACD_12_26_9 | MACDh_12_26_9 | MACDs_12_26_9 | macd_trend | RSI_14 | overbought | oversold | RSI_trend | return | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| timestamp | ||||||||||||||||

| 2017-08-26 00:00:00 | 53 | 2017-08-26 00:00:00 | 327.24 | 332.27 | 323.41 | 323.46 | 569.57801 | 5.218425 | -0.144303 | 5.362728 | False | 53.515087 | NaN | NaN | 1.0 | 0.050022 |

| 2017-08-27 16:00:00 | 63 | 2017-08-27 16:00:00 | 335.04 | 341.47 | 332.97 | 339.64 | 795.13177 | 5.146901 | 0.285160 | 4.861741 | True | 68.589301 | NaN | NaN | 1.0 | 0.131934 |

| 2017-08-31 16:00:00 | 87 | 2017-08-31 16:00:00 | 384.38 | 387.39 | 383.13 | 384.45 | 878.88372 | 12.619776 | -0.009218 | 12.628994 | False | 73.658395 | NaN | NaN | 1.0 | -0.172168 |

| 2017-09-05 16:00:00 | 117 | 2017-09-05 16:00:00 | 290.07 | 321.52 | 285.94 | 318.26 | 677.80125 | -17.420385 | 0.985630 | -18.406015 | True | 48.964468 | NaN | NaN | -1.0 | -0.076070 |

| 2017-09-08 12:00:00 | 134 | 2017-09-08 12:00:00 | 330.10 | 331.57 | 272.00 | 294.05 | 2343.12862 | -1.422169 | -0.756305 | -0.665864 | False | 36.802842 | NaN | NaN | -1.0 | 0.026220 |

| … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … |

| 2023-03-03 00:00:00 | 12139 | 2023-03-03 00:00:00 | 1647.86 | 1649.25 | 1544.39 | 1565.44 | 317798.34160 | -2.231587 | -5.079240 | 2.847653 | False | 34.504987 | NaN | NaN | -1.0 | 0.001955 |

| 2023-03-05 08:00:00 | 12153 | 2023-03-05 08:00:00 | 1568.61 | 1573.07 | 1564.03 | 1568.50 | 32527.56420 | -16.383615 | 0.212968 | -16.596583 | True | 38.888106 | NaN | NaN | -1.0 | -0.023028 |

| 2023-03-08 20:00:00 | 12174 | 2023-03-08 20:00:00 | 1552.72 | 1561.29 | 1523.61 | 1532.38 | 128310.87040 | -9.161005 | -0.786086 | -8.374919 | False | 32.613518 | NaN | NaN | -1.0 | -0.054269 |

| 2023-03-11 16:00:00 | 12191 | 2023-03-11 16:00:00 | 1428.00 | 1457.04 | 1422.32 | 1449.22 | 180365.58850 | -32.769032 | 1.859142 | -34.628174 | True | 42.608536 | NaN | NaN | -1.0 | 0.127531 |

| 2023-03-15 12:00:00 | 12214 | 2023-03-15 12:00:00 | 1679.91 | 1698.29 | 1625.56 | 1634.04 | 313571.19570 | 46.865502 | -3.715414 | 50.580916 | False | 52.346900 | NaN | NaN | 1.0 | NaN |

921 rows × 16 columns

Clean data

signaled=signaled.iloc[:-1]

signaled| index | timestamp | open | high | low | close | volume | MACD_12_26_9 | MACDh_12_26_9 | MACDs_12_26_9 | macd_trend | RSI_14 | overbought | oversold | RSI_trend | return | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| timestamp | ||||||||||||||||

| 2017-08-26 00:00:00 | 53 | 2017-08-26 00:00:00 | 327.24 | 332.27 | 323.41 | 323.46 | 569.57801 | 5.218425 | -0.144303 | 5.362728 | False | 53.515087 | NaN | NaN | 1.0 | 0.050022 |

| 2017-08-27 16:00:00 | 63 | 2017-08-27 16:00:00 | 335.04 | 341.47 | 332.97 | 339.64 | 795.13177 | 5.146901 | 0.285160 | 4.861741 | True | 68.589301 | NaN | NaN | 1.0 | 0.131934 |

| 2017-08-31 16:00:00 | 87 | 2017-08-31 16:00:00 | 384.38 | 387.39 | 383.13 | 384.45 | 878.88372 | 12.619776 | -0.009218 | 12.628994 | False | 73.658395 | NaN | NaN | 1.0 | -0.172168 |

| 2017-09-05 16:00:00 | 117 | 2017-09-05 16:00:00 | 290.07 | 321.52 | 285.94 | 318.26 | 677.80125 | -17.420385 | 0.985630 | -18.406015 | True | 48.964468 | NaN | NaN | -1.0 | -0.076070 |

| 2017-09-08 12:00:00 | 134 | 2017-09-08 12:00:00 | 330.10 | 331.57 | 272.00 | 294.05 | 2343.12862 | -1.422169 | -0.756305 | -0.665864 | False | 36.802842 | NaN | NaN | -1.0 | 0.026220 |

| … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … |

| 2023-03-02 16:00:00 | 12137 | 2023-03-02 16:00:00 | 1628.31 | 1652.48 | 1621.45 | 1648.48 | 78007.64970 | 4.138191 | 0.061488 | 4.076702 | True | 53.188566 | NaN | NaN | 1.0 | -0.050374 |

| 2023-03-03 00:00:00 | 12139 | 2023-03-03 00:00:00 | 1647.86 | 1649.25 | 1544.39 | 1565.44 | 317798.34160 | -2.231587 | -5.079240 | 2.847653 | False | 34.504987 | NaN | NaN | -1.0 | 0.001955 |

| 2023-03-05 08:00:00 | 12153 | 2023-03-05 08:00:00 | 1568.61 | 1573.07 | 1564.03 | 1568.50 | 32527.56420 | -16.383615 | 0.212968 | -16.596583 | True | 38.888106 | NaN | NaN | -1.0 | -0.023028 |

| 2023-03-08 20:00:00 | 12174 | 2023-03-08 20:00:00 | 1552.72 | 1561.29 | 1523.61 | 1532.38 | 128310.87040 | -9.161005 | -0.786086 | -8.374919 | False | 32.613518 | NaN | NaN | -1.0 | -0.054269 |

| 2023-03-11 16:00:00 | 12191 | 2023-03-11 16:00:00 | 1428.00 | 1457.04 | 1422.32 | 1449.22 | 180365.58850 | -32.769032 | 1.859142 | -34.628174 | True | 42.608536 | NaN | NaN | -1.0 | 0.127531 |

920 rows × 16 columns

signaled_filter=signaled[['close','macd_trend','overbought','oversold','RSI_trend','MACDs_12_26_9','MACD_12_26_9','RSI_14','return',]]Label y: profit = 1, loss = -1, and nonprofit = 0

signaled_filter.loc[signaled_filter['return']>0,'y']=1

signaled_filter.loc[signaled_filter['return']<0,'y']=-1

signaled_filter.loc[signaled_filter['return']==0,'y']=0Clean data

signaled_filter = signaled_filter.fillna(0)

signaled_filter| close | macd_trend | overbought | oversold | RSI_trend | MACDs_12_26_9 | MACD_12_26_9 | RSI_14 | return | y | |

|---|---|---|---|---|---|---|---|---|---|---|

| timestamp | ||||||||||

| 2017-08-26 00:00:00 | 323.46 | False | 0.0 | 0.0 | 1.0 | 5.362728 | 5.218425 | 53.515087 | 0.050022 | 1.0 |

| 2017-08-27 16:00:00 | 339.64 | True | 0.0 | 0.0 | 1.0 | 4.861741 | 5.146901 | 68.589301 | 0.131934 | 1.0 |

| 2017-08-31 16:00:00 | 384.45 | False | 0.0 | 0.0 | 1.0 | 12.628994 | 12.619776 | 73.658395 | -0.172168 | -1.0 |

| 2017-09-05 16:00:00 | 318.26 | True | 0.0 | 0.0 | -1.0 | -18.406015 | -17.420385 | 48.964468 | -0.076070 | -1.0 |

| 2017-09-08 12:00:00 | 294.05 | False | 0.0 | 0.0 | -1.0 | -0.665864 | -1.422169 | 36.802842 | 0.026220 | 1.0 |

| … | … | … | … | … | … | … | … | … | … | … |

| 2023-03-02 16:00:00 | 1648.48 | True | 0.0 | 0.0 | 1.0 | 4.076702 | 4.138191 | 53.188566 | -0.050374 | -1.0 |

| 2023-03-03 00:00:00 | 1565.44 | False | 0.0 | 0.0 | -1.0 | 2.847653 | -2.231587 | 34.504987 | 0.001955 | 1.0 |

| 2023-03-05 08:00:00 | 1568.50 | True | 0.0 | 0.0 | -1.0 | -16.596583 | -16.383615 | 38.888106 | -0.023028 | -1.0 |

| 2023-03-08 20:00:00 | 1532.38 | False | 0.0 | 0.0 | -1.0 | -8.374919 | -9.161005 | 32.613518 | -0.054269 | -1.0 |

| 2023-03-11 16:00:00 | 1449.22 | True | 0.0 | 0.0 | -1.0 | -34.628174 | -32.769032 | 42.608536 | 0.127531 | 1.0 |

920 rows × 10 columns

Separate features and target

#my_features to traning = ['macd_trend','overbought','oversold','RSI_trend','MACDs_12_26_9','MACD_12_26_9','RSI_14']

X = signaled_filter.iloc[:,1:-2]

y = signaled_filter.iloc[:,-1]X| macd_trend | overbought | oversold | RSI_trend | MACDs_12_26_9 | MACD_12_26_9 | RSI_14 | |

|---|---|---|---|---|---|---|---|

| timestamp | |||||||

| 2017-08-26 00:00:00 | False | 0.0 | 0.0 | 1.0 | 5.362728 | 5.218425 | 53.515087 |

| 2017-08-27 16:00:00 | True | 0.0 | 0.0 | 1.0 | 4.861741 | 5.146901 | 68.589301 |

| 2017-08-31 16:00:00 | False | 0.0 | 0.0 | 1.0 | 12.628994 | 12.619776 | 73.658395 |

| 2017-09-05 16:00:00 | True | 0.0 | 0.0 | -1.0 | -18.406015 | -17.420385 | 48.964468 |

| 2017-09-08 12:00:00 | False | 0.0 | 0.0 | -1.0 | -0.665864 | -1.422169 | 36.802842 |

| … | … | … | … | … | … | … | … |

| 2023-03-02 16:00:00 | True | 0.0 | 0.0 | 1.0 | 4.076702 | 4.138191 | 53.188566 |

| 2023-03-03 00:00:00 | False | 0.0 | 0.0 | -1.0 | 2.847653 | -2.231587 | 34.504987 |

| 2023-03-05 08:00:00 | True | 0.0 | 0.0 | -1.0 | -16.596583 | -16.383615 | 38.888106 |

| 2023-03-08 20:00:00 | False | 0.0 | 0.0 | -1.0 | -8.374919 | -9.161005 | 32.613518 |

| 2023-03-11 16:00:00 | True | 0.0 | 0.0 | -1.0 | -34.628174 | -32.769032 | 42.608536 |

920 rows × 7 columns

Split data into training and testing sets

from 920 data will use data to traning 700 data and test 100 data and split data to test with machine learning model 120 data how it working

X_train = X.iloc[:700]

y_train = y.iloc[:700]

X_test = X.iloc[700:800]

y_test = y.iloc[700:800]Now, let’s import the Random Forest model and evaluate its performance.

Import machine learning model RandomForestRegressor and GridSearchCV for finding best parameter of machine learning and

from sklearn.model_selection import train_test_split

from sklearn.ensemble import (RandomForestRegressor,

RandomForestClassifier)

from sklearn.metrics import (mean_squared_error,

r2_score,

mean_absolute_error,

mean_absolute_percentage_error,

accuracy_score,

precision_score,

recall_score,

f1_score)

from sklearn.model_selection import (GridSearchCV,

TimeSeriesSplit)Split data (75% for training, 25% for testing)

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.25, random_state=0, shuffle=False)Hyperparameter Tuning with GridSearchCV

First, we define the Random Forest parameters for tuning with GridSearchCV:

rf_params = {

'n_estimators': [100,200,300],

'max_depth': np.arange(3,6,1),

'min_samples_leaf': [1,2,5,10],

'bootstrap': [True, False],

'max_features': [1, 2],

}

Next, we use TimeSeriesSplit to split the data and obtain the best parameters using GridSearchCV:

# initial TimeSeriesSplit = 5 it mean split to 5

tscv = TimeSeriesSplit(n_splits = 5)

# use grid Search parameter

rf_regr = GridSearchCV(RandomForestClassifier(random_state=0), rf_params, cv=tscv, n_jobs=-1)

grid_result = rf_regr.fit(X_train, y_train)

# we will see the result in this section

print('Best Score: ', grid_result.best_score_)

print('Best Params: ', grid_result.best_params_)

Best Score: 0.5982758620689654

Best Params: {'bootstrap': True, 'max_depth': 3, 'max_features': 2, 'min_samples_leaf': 2, 'n_estimators': 100}

Creating the RandomForestClassifier

After obtaining the best parameters from GridSearchCV, we create the RandomForestClassifier:

clf =RandomForestClassifier(

max_depth=grid_result.best_params_['max_depth'],

n_estimators=grid_result.best_params_['n_estimators'],

max_features=grid_result.best_params_['max_features'],

min_samples_leaf=grid_result.best_params_['min_samples_leaf'],

random_state=0)

clf.fit(X_train,y_train)

# output

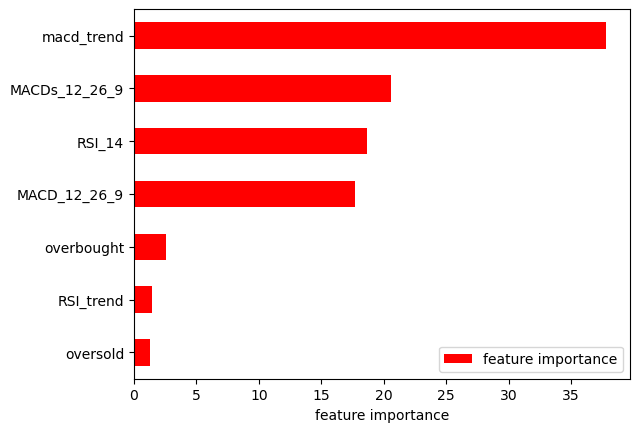

RandomForestClassifier(max_depth=3, max_features=2, min_samples_leaf=2,random_state=0)Feature Importance Analysis

We visualize the feature importance to understand the impact of each feature on the model:

Importance = pd.DataFrame({'feature importance':clf.feature_importances_*100}, index=X_train.columns)

Importance.sort_values('feature importance', axis=0, ascending=True).plot(kind='barh', color='r')

plt.xlabel('feature importance')

preview predict and actual with dataframe

y_pred = clf.predict(X_test)pd.DataFrame({'actual': y_test,

'predict': y_pred})| actual | predict | |

|---|---|---|

| timestamp | ||

| 2021-11-04 08:00:00 | 1.0 | 1.0 |

| 2021-11-07 08:00:00 | 1.0 | -1.0 |

| 2021-11-09 20:00:00 | -1.0 | 1.0 |

| 2021-11-15 00:00:00 | -1.0 | -1.0 |

| 2021-11-15 20:00:00 | -1.0 | 1.0 |

| … | … | … |

| 2022-05-13 04:00:00 | -1.0 | -1.0 |

| 2022-05-18 12:00:00 | 1.0 | 1.0 |

| 2022-05-19 16:00:00 | -1.0 | -1.0 |

| 2022-05-21 00:00:00 | 1.0 | 1.0 |

| 2022-05-21 04:00:00 | 1.0 | -1.0 |

100 rows × 2 columns

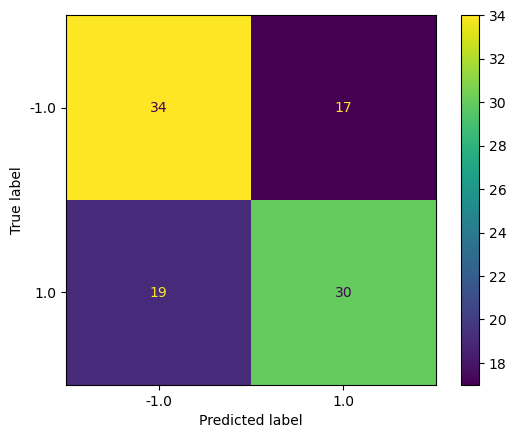

Create Confusion Matrix to see how accuracy from this model

from sklearn.metrics import plot_confusion_matrix

plot_confusion_matrix(clf,X_test,y_test)

from sklearn import metricsModel Evaluation

We compare the predicted values with the actual values using a confusion matrix and calculate the accuracy, precision, recall, and F1 score:

print('Accuracy:',metrics.accuracy_score(y_test,y_pred))

print('Precision:',metrics.precision_score(y_test,y_pred))

print('Recall:',metrics.recall_score(y_test,y_pred))

print('F1 Score:',metrics.f1_score(y_test,y_pred))

Accuracy: 0.64

Precision: 0.6382978723404256

Recall: 0.6122448979591837

F1 Score: 0.625

test with real data

X_live = X.iloc[100:]

X_live| macd_trend | overbought | oversold | RSI_trend | MACDs_12_26_9 | MACD_12_26_9 | RSI_14 | |

|---|---|---|---|---|---|---|---|

| timestamp | |||||||

| 2018-04-22 00:00:00 | False | 0.0 | 0.0 | 1.0 | 23.126038 | 22.931511 | 62.966387 |

| 2018-04-22 08:00:00 | True | 0.0 | 0.0 | 1.0 | 23.071536 | 23.234708 | 69.677206 |

| 2018-04-23 08:00:00 | False | 0.0 | 0.0 | 1.0 | 23.713086 | 23.642522 | 66.992778 |

| 2018-04-24 00:00:00 | True | 0.0 | 0.0 | 1.0 | 23.458020 | 23.950860 | 72.530878 |

| 2018-04-25 04:00:00 | False | 0.0 | 0.0 | 1.0 | 27.296406 | 25.439792 | 56.633962 |

| … | … | … | … | … | … | … | … |

| 2023-03-02 16:00:00 | True | 0.0 | 0.0 | 1.0 | 4.076702 | 4.138191 | 53.188566 |

| 2023-03-03 00:00:00 | False | 0.0 | 0.0 | -1.0 | 2.847653 | -2.231587 | 34.504987 |

| 2023-03-05 08:00:00 | True | 0.0 | 0.0 | -1.0 | -16.596583 | -16.383615 | 38.888106 |

| 2023-03-08 20:00:00 | False | 0.0 | 0.0 | -1.0 | -8.374919 | -9.161005 | 32.613518 |

| 2023-03-11 16:00:00 | True | 0.0 | 0.0 | -1.0 | -34.628174 | -32.769032 | 42.608536 |

820 rows × 7 columns

test_live = signaled[100:].copy()

test_live| index | timestamp | open | high | low | close | volume | MACD_12_26_9 | MACDh_12_26_9 | MACDs_12_26_9 | macd_trend | RSI_14 | overbought | oversold | RSI_trend | return | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| timestamp | ||||||||||||||||

| 2018-04-22 00:00:00 | 1481 | 2018-04-22 00:00:00 | 604.87 | 606.00 | 589.00 | 600.14 | 17037.36423 | 22.931511 | -0.194527 | 23.126038 | False | 62.966387 | NaN | NaN | 1.0 | 0.041657 |

| 2018-04-22 08:00:00 | 1483 | 2018-04-22 08:00:00 | 611.80 | 633.56 | 611.03 | 625.14 | 26165.67594 | 23.234708 | 0.163172 | 23.071536 | True | 69.677206 | NaN | NaN | 1.0 | 0.019548 |

| 2018-04-23 08:00:00 | 1489 | 2018-04-23 08:00:00 | 641.10 | 642.00 | 630.42 | 637.36 | 15391.27247 | 23.642522 | -0.070564 | 23.713086 | False | 66.992778 | NaN | NaN | 1.0 | 0.049752 |

| 2018-04-24 00:00:00 | 1493 | 2018-04-24 00:00:00 | 644.58 | 673.20 | 643.76 | 669.07 | 31087.69471 | 23.950860 | 0.492840 | 23.458020 | True | 72.530878 | NaN | NaN | 1.0 | -0.011763 |

| 2018-04-25 04:00:00 | 1500 | 2018-04-25 04:00:00 | 654.00 | 669.00 | 624.00 | 661.20 | 67160.89082 | 25.439792 | -1.856614 | 27.296406 | False | 56.633962 | NaN | NaN | 1.0 | 0.028947 |

| … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … |

| 2023-03-02 16:00:00 | 12137 | 2023-03-02 16:00:00 | 1628.31 | 1652.48 | 1621.45 | 1648.48 | 78007.64970 | 4.138191 | 0.061488 | 4.076702 | True | 53.188566 | NaN | NaN | 1.0 | -0.050374 |

| 2023-03-03 00:00:00 | 12139 | 2023-03-03 00:00:00 | 1647.86 | 1649.25 | 1544.39 | 1565.44 | 317798.34160 | -2.231587 | -5.079240 | 2.847653 | False | 34.504987 | NaN | NaN | -1.0 | 0.001955 |

| 2023-03-05 08:00:00 | 12153 | 2023-03-05 08:00:00 | 1568.61 | 1573.07 | 1564.03 | 1568.50 | 32527.56420 | -16.383615 | 0.212968 | -16.596583 | True | 38.888106 | NaN | NaN | -1.0 | -0.023028 |

| 2023-03-08 20:00:00 | 12174 | 2023-03-08 20:00:00 | 1552.72 | 1561.29 | 1523.61 | 1532.38 | 128310.87040 | -9.161005 | -0.786086 | -8.374919 | False | 32.613518 | NaN | NaN | -1.0 | -0.054269 |

| 2023-03-11 16:00:00 | 12191 | 2023-03-11 16:00:00 | 1428.00 | 1457.04 | 1422.32 | 1449.22 | 180365.58850 | -32.769032 | 1.859142 | -34.628174 | True | 42.608536 | NaN | NaN | -1.0 | 0.127531 |

820 rows × 16 columns

test_live['signal']=clf.predict(X_live)

test_live| index | timestamp | open | high | low | close | volume | MACD_12_26_9 | MACDh_12_26_9 | MACDs_12_26_9 | macd_trend | RSI_14 | overbought | oversold | RSI_trend | return | signal | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| timestamp | |||||||||||||||||

| 2018-04-22 00:00:00 | 1481 | 2018-04-22 00:00:00 | 604.87 | 606.00 | 589.00 | 600.14 | 17037.36423 | 22.931511 | -0.194527 | 23.126038 | False | 62.966387 | NaN | NaN | 1.0 | 0.041657 | 1.0 |

| 2018-04-22 08:00:00 | 1483 | 2018-04-22 08:00:00 | 611.80 | 633.56 | 611.03 | 625.14 | 26165.67594 | 23.234708 | 0.163172 | 23.071536 | True | 69.677206 | NaN | NaN | 1.0 | 0.019548 | -1.0 |

| 2018-04-23 08:00:00 | 1489 | 2018-04-23 08:00:00 | 641.10 | 642.00 | 630.42 | 637.36 | 15391.27247 | 23.642522 | -0.070564 | 23.713086 | False | 66.992778 | NaN | NaN | 1.0 | 0.049752 | 1.0 |

| 2018-04-24 00:00:00 | 1493 | 2018-04-24 00:00:00 | 644.58 | 673.20 | 643.76 | 669.07 | 31087.69471 | 23.950860 | 0.492840 | 23.458020 | True | 72.530878 | NaN | NaN | 1.0 | -0.011763 | -1.0 |

| 2018-04-25 04:00:00 | 1500 | 2018-04-25 04:00:00 | 654.00 | 669.00 | 624.00 | 661.20 | 67160.89082 | 25.439792 | -1.856614 | 27.296406 | False | 56.633962 | NaN | NaN | 1.0 | 0.028947 | 1.0 |

| … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … |

| 2023-03-02 16:00:00 | 12137 | 2023-03-02 16:00:00 | 1628.31 | 1652.48 | 1621.45 | 1648.48 | 78007.64970 | 4.138191 | 0.061488 | 4.076702 | True | 53.188566 | NaN | NaN | 1.0 | -0.050374 | -1.0 |

| 2023-03-03 00:00:00 | 12139 | 2023-03-03 00:00:00 | 1647.86 | 1649.25 | 1544.39 | 1565.44 | 317798.34160 | -2.231587 | -5.079240 | 2.847653 | False | 34.504987 | NaN | NaN | -1.0 | 0.001955 | 1.0 |

| 2023-03-05 08:00:00 | 12153 | 2023-03-05 08:00:00 | 1568.61 | 1573.07 | 1564.03 | 1568.50 | 32527.56420 | -16.383615 | 0.212968 | -16.596583 | True | 38.888106 | NaN | NaN | -1.0 | -0.023028 | -1.0 |

| 2023-03-08 20:00:00 | 12174 | 2023-03-08 20:00:00 | 1552.72 | 1561.29 | 1523.61 | 1532.38 | 128310.87040 | -9.161005 | -0.786086 | -8.374919 | False | 32.613518 | NaN | NaN | -1.0 | -0.054269 | 1.0 |

| 2023-03-11 16:00:00 | 12191 | 2023-03-11 16:00:00 | 1428.00 | 1457.04 | 1422.32 | 1449.22 | 180365.58850 | -32.769032 | 1.859142 | -34.628174 | True | 42.608536 | NaN | NaN | -1.0 | 0.127531 | -1.0 |

820 rows × 17 columns

change signal ml from -1 1. to True False cause will use to vectorbt backtest

test_live['signal']=test_live['signal'].apply(lambda x:True if x==1 else False)

test_live

| index | timestamp | open | high | low | close | volume | MACD_12_26_9 | MACDh_12_26_9 | MACDs_12_26_9 | macd_trend | RSI_14 | overbought | oversold | RSI_trend | return | signal | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| timestamp | |||||||||||||||||

| 2018-04-22 00:00:00 | 1481 | 2018-04-22 00:00:00 | 604.87 | 606.00 | 589.00 | 600.14 | 17037.36423 | 22.931511 | -0.194527 | 23.126038 | False | 62.966387 | NaN | NaN | 1.0 | 0.041657 | True |

| 2018-04-22 08:00:00 | 1483 | 2018-04-22 08:00:00 | 611.80 | 633.56 | 611.03 | 625.14 | 26165.67594 | 23.234708 | 0.163172 | 23.071536 | True | 69.677206 | NaN | NaN | 1.0 | 0.019548 | False |

| 2018-04-23 08:00:00 | 1489 | 2018-04-23 08:00:00 | 641.10 | 642.00 | 630.42 | 637.36 | 15391.27247 | 23.642522 | -0.070564 | 23.713086 | False | 66.992778 | NaN | NaN | 1.0 | 0.049752 | True |

| 2018-04-24 00:00:00 | 1493 | 2018-04-24 00:00:00 | 644.58 | 673.20 | 643.76 | 669.07 | 31087.69471 | 23.950860 | 0.492840 | 23.458020 | True | 72.530878 | NaN | NaN | 1.0 | -0.011763 | False |

| 2018-04-25 04:00:00 | 1500 | 2018-04-25 04:00:00 | 654.00 | 669.00 | 624.00 | 661.20 | 67160.89082 | 25.439792 | -1.856614 | 27.296406 | False | 56.633962 | NaN | NaN | 1.0 | 0.028947 | True |

| … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … |

| 2023-03-02 16:00:00 | 12137 | 2023-03-02 16:00:00 | 1628.31 | 1652.48 | 1621.45 | 1648.48 | 78007.64970 | 4.138191 | 0.061488 | 4.076702 | True | 53.188566 | NaN | NaN | 1.0 | -0.050374 | False |

| 2023-03-03 00:00:00 | 12139 | 2023-03-03 00:00:00 | 1647.86 | 1649.25 | 1544.39 | 1565.44 | 317798.34160 | -2.231587 | -5.079240 | 2.847653 | False | 34.504987 | NaN | NaN | -1.0 | 0.001955 | True |

| 2023-03-05 08:00:00 | 12153 | 2023-03-05 08:00:00 | 1568.61 | 1573.07 | 1564.03 | 1568.50 | 32527.56420 | -16.383615 | 0.212968 | -16.596583 | True | 38.888106 | NaN | NaN | -1.0 | -0.023028 | False |

| 2023-03-08 20:00:00 | 12174 | 2023-03-08 20:00:00 | 1552.72 | 1561.29 | 1523.61 | 1532.38 | 128310.87040 | -9.161005 | -0.786086 | -8.374919 | False | 32.613518 | NaN | NaN | -1.0 | -0.054269 | True |

| 2023-03-11 16:00:00 | 12191 | 2023-03-11 16:00:00 | 1428.00 | 1457.04 | 1422.32 | 1449.22 | 180365.58850 | -32.769032 | 1.859142 | -34.628174 | True | 42.608536 | NaN | NaN | -1.0 | 0.127531 | False |

820 rows × 17 columns

Testing the Model on Live Data

We test the model on live data to validate its performance and use vectorbt to backtest the results.

Filter the prediction data frame based on the live test data

time_predict =test_live.index[0]

df_predict=df.copy()df_predict['timestamp'] = pd.to_datetime(df['timestamp'], unit='ms')

df_predict.reset_index(inplace=True)

df_predict.set_index(df_predict['timestamp'],inplace=True)

df_predict| index | timestamp | open | high | low | close | volume | |

|---|---|---|---|---|---|---|---|

| timestamp | |||||||

| 2017-08-17 04:00:00 | 0 | 2017-08-17 04:00:00 | 301.13 | 307.96 | 298.00 | 307.96 | 1561.95305 |

| 2017-08-17 08:00:00 | 1 | 2017-08-17 08:00:00 | 307.95 | 312.00 | 307.00 | 308.95 | 1177.71088 |

| 2017-08-17 12:00:00 | 2 | 2017-08-17 12:00:00 | 308.95 | 310.51 | 303.56 | 307.06 | 1882.05267 |

| 2017-08-17 16:00:00 | 3 | 2017-08-17 16:00:00 | 307.74 | 312.18 | 298.21 | 301.60 | 1208.05192 |

| 2017-08-17 20:00:00 | 4 | 2017-08-17 20:00:00 | 301.60 | 310.85 | 299.01 | 302.00 | 1200.94182 |

| … | … | … | … | … | … | … | … |

| 2023-03-16 12:00:00 | 12220 | 2023-03-16 12:00:00 | 1660.37 | 1666.73 | 1635.96 | 1663.06 | 129192.79690 |

| 2023-03-16 16:00:00 | 12221 | 2023-03-16 16:00:00 | 1663.06 | 1691.42 | 1652.88 | 1679.64 | 113369.52090 |

| 2023-03-16 20:00:00 | 12222 | 2023-03-16 20:00:00 | 1679.64 | 1681.78 | 1652.53 | 1673.73 | 76922.01860 |

| 2023-03-17 00:00:00 | 12223 | 2023-03-17 00:00:00 | 1673.73 | 1725.00 | 1662.65 | 1708.62 | 166034.43070 |

| 2023-03-17 04:00:00 | 12224 | 2023-03-17 04:00:00 | 1708.62 | 1730.99 | 1696.37 | 1715.56 | 103495.68750 |

12225 rows × 7 columns

df_predict=df_predict.loc[time_predict:,:'close']

df_predict| index | timestamp | open | high | low | close | |

|---|---|---|---|---|---|---|

| timestamp | ||||||

| 2018-04-22 00:00:00 | 1481 | 2018-04-22 00:00:00 | 604.87 | 606.00 | 589.00 | 600.14 |

| 2018-04-22 04:00:00 | 1482 | 2018-04-22 04:00:00 | 600.22 | 612.49 | 599.00 | 611.80 |

| 2018-04-22 08:00:00 | 1483 | 2018-04-22 08:00:00 | 611.80 | 633.56 | 611.03 | 625.14 |

| 2018-04-22 12:00:00 | 1484 | 2018-04-22 12:00:00 | 625.20 | 641.00 | 614.31 | 634.46 |

| 2018-04-22 16:00:00 | 1485 | 2018-04-22 16:00:00 | 634.46 | 643.49 | 630.00 | 636.58 |

| … | … | … | … | … | … | … |

| 2023-03-16 12:00:00 | 12220 | 2023-03-16 12:00:00 | 1660.37 | 1666.73 | 1635.96 | 1663.06 |

| 2023-03-16 16:00:00 | 12221 | 2023-03-16 16:00:00 | 1663.06 | 1691.42 | 1652.88 | 1679.64 |

| 2023-03-16 20:00:00 | 12222 | 2023-03-16 20:00:00 | 1679.64 | 1681.78 | 1652.53 | 1673.73 |

| 2023-03-17 00:00:00 | 12223 | 2023-03-17 00:00:00 | 1673.73 | 1725.00 | 1662.65 | 1708.62 |

| 2023-03-17 04:00:00 | 12224 | 2023-03-17 04:00:00 | 1708.62 | 1730.99 | 1696.37 | 1715.56 |

10744 rows × 6 columns

test_live['signal']

timestamp

2018-04-22 00:00:00 True

2018-04-22 08:00:00 False

2018-04-23 08:00:00 True

2018-04-24 00:00:00 False

2018-04-25 04:00:00 True

...

2023-03-02 16:00:00 False

2023-03-03 00:00:00 True

2023-03-05 08:00:00 False

2023-03-08 20:00:00 True

2023-03-11 16:00:00 False

Name: signal, Length: 820, dtype: bool

Add the signal from the machine learning model to the live data

df_predict = df_predict.join(test_live['signal'])

df_predict =df_predict.fillna(method='ffill')df_predict| index | timestamp | open | high | low | close | signal | |

|---|---|---|---|---|---|---|---|

| timestamp | |||||||

| 2018-04-22 00:00:00 | 1481 | 2018-04-22 00:00:00 | 604.87 | 606.00 | 589.00 | 600.14 | True |

| 2018-04-22 04:00:00 | 1482 | 2018-04-22 04:00:00 | 600.22 | 612.49 | 599.00 | 611.80 | True |

| 2018-04-22 08:00:00 | 1483 | 2018-04-22 08:00:00 | 611.80 | 633.56 | 611.03 | 625.14 | False |

| 2018-04-22 12:00:00 | 1484 | 2018-04-22 12:00:00 | 625.20 | 641.00 | 614.31 | 634.46 | False |

| 2018-04-22 16:00:00 | 1485 | 2018-04-22 16:00:00 | 634.46 | 643.49 | 630.00 | 636.58 | False |

| … | … | … | … | … | … | … | … |

| 2023-03-16 12:00:00 | 12220 | 2023-03-16 12:00:00 | 1660.37 | 1666.73 | 1635.96 | 1663.06 | False |

| 2023-03-16 16:00:00 | 12221 | 2023-03-16 16:00:00 | 1663.06 | 1691.42 | 1652.88 | 1679.64 | False |

| 2023-03-16 20:00:00 | 12222 | 2023-03-16 20:00:00 | 1679.64 | 1681.78 | 1652.53 | 1673.73 | False |

| 2023-03-17 00:00:00 | 12223 | 2023-03-17 00:00:00 | 1673.73 | 1725.00 | 1662.65 | 1708.62 | False |

| 2023-03-17 04:00:00 | 12224 | 2023-03-17 04:00:00 | 1708.62 | 1730.99 | 1696.37 | 1715.56 | False |

10744 rows × 7 columns

Create vectorbt signals

signal_vectorbt_ml_turning = df_predict.ta.tsignals(df_predict.signal,

asbool=True,append=True)

signal_vectorbt_ml_turning.loc[signal_vectorbt_ml_turning['TS_Trades']!=0]will see the result vectorbt signal

| TS_Trends | TS_Trades | TS_Entries | TS_Exits | |

|---|---|---|---|---|

| timestamp | ||||

| 2018-04-22 08:00:00 | False | -1 | False | True |

| 2018-04-23 08:00:00 | True | 1 | True | False |

| 2018-04-24 00:00:00 | False | -1 | False | True |

| 2018-04-25 04:00:00 | True | 1 | True | False |

| 2018-04-27 08:00:00 | False | -1 | False | True |

| … | … | … | … | … |

| 2023-03-02 16:00:00 | False | -1 | False | True |

| 2023-03-03 00:00:00 | True | 1 | True | False |

| 2023-03-05 08:00:00 | False | -1 | False | True |

| 2023-03-08 20:00:00 | True | 1 | True | False |

| 2023-03-11 16:00:00 | False | -1 | False | True |

783 rows × 4 columns

Use vectorbt Portfolio from_signals to backtest the strategy

port_ml_turning = vbt.Portfolio.from_signals(df_predict.open,entries=signal_vectorbt_ml_turning.TS_Exits,exits=signal_vectorbt_ml_turning.TS_Entries,freq = '4h',init_cash = 1000,size=0.1,fees = 0.0002,direction=2,slippage = 0.005,)

#Plot the portfolio

port_ml_turning.plot().show()

Display the portfolio statistics

port_ml_turning.stats()

Start 2018-04-22 00:00:00

End 2023-03-17 04:00:00

Period 447 days 16:00:00

Start Value 1000.0

End Value 2802.131168

Total Return [%] 180.213117

Benchmark Return [%] 182.477227

Max Gross Exposure [%] 27.505487

Total Fees Paid 36.027332

Max Drawdown [%] 13.663183

Max Drawdown Duration 12 days 00:00:00

Total Trades 783

Total Closed Trades 782

Total Open Trades 1

Open Trade PnL 27.319297

Win Rate [%] 51.918159

Best Trade [%] 57.756017

Worst Trade [%] -22.688176

Avg Winning Trade [%] 6.603421

Avg Losing Trade [%] -2.416791

Avg Winning Trade Duration 0 days 17:53:56.453201970

Avg Losing Trade Duration 0 days 09:09:05.744680851

Profit Factor 2.443637

Expectancy 2.26958

Sharpe Ratio 4.818487

Calmar Ratio 9.636257

Omega Ratio 1.234305

Sortino Ratio 7.252599

dtype: object