What Idea about Stock Analysis and Predicting chart ?

Introduction: In this article, we will explore how to perform stock analysis using Python. We will import and merge multiple datasets, including historical stock prices, earnings per share (EPS), and GDP data. We will then use linear regression to predict stock returns based on historical data. Finally, we will visualize the results using various libraries like pandas, matplotlib, numpy, and seaborn.

importing the necessary libraries

import pandas as pd

import matplotlib.pyplot as plt

import numpy as np

import seaborn as snsImport Dataframe from Excel

Now, we will read the data from Excel files and store them in pandas DataFrames:

data_set = pd.read_excel('set.xlsx',index_col=0)

data_set_eps = pd.read_excel('set_eps.xlsx',index_col=0)

data_gdpq = pd.read_excel('gdpq.xlsx',engine= 'openpyxl',index_col=0)After importing the data, we can display the DataFrames to see what they look like:

data_setwe will see dataframe like this

| Prior | Open | High | Low | Close | PE | |

|---|---|---|---|---|---|---|

| Date | ||||||

| 2016-01-04 | 1288.02 | 1286.29 | 1286.36 | 1260.96 | 1263.41 | 22.12 |

| 2016-01-05 | 1263.41 | 1267.20 | 1270.07 | 1251.87 | 1253.34 | 21.99 |

| 2016-01-06 | 1253.34 | 1249.82 | 1260.88 | 1247.89 | 1260.04 | 22.10 |

| 2016-01-07 | 1260.04 | 1237.81 | 1244.04 | 1224.83 | 1224.83 | 21.46 |

| 2016-01-08 | 1224.83 | 1232.31 | 1246.70 | 1228.18 | 1244.18 | 21.81 |

| … | … | … | … | … | … | … |

| 2021-10-28 | 1627.61 | 1626.27 | 1632.30 | 1622.56 | 1624.31 | 20.81 |

| 2021-10-29 | 1624.31 | 1627.01 | 1629.25 | 1619.14 | 1623.43 | 21.02 |

| 2021-11-01 | 1623.43 | 1627.54 | 1632.73 | 1611.39 | 1613.78 | 20.89 |

| 2021-11-02 | 1613.78 | 1616.86 | 1621.69 | 1608.64 | 1617.89 | 20.96 |

| 2021-11-03 | 1617.89 | 1620.90 | 1623.08 | 1607.72 | 1611.92 | 20.87 |

1422 rows × 6 columns

data_set_eps| Prior | Open | High | Low | Close | PE | EPS | |

|---|---|---|---|---|---|---|---|

| Date | |||||||

| 2021-11-03 | 1617.89 | 1620.90 | 1623.08 | 1607.72 | 1611.92 | 19.3909 | 83.1235 |

| 2021-11-02 | 1613.78 | 1616.86 | 1621.69 | 1608.64 | 1617.89 | 19.4637 | 83.1246 |

| 2021-11-01 | 1623.43 | 1627.54 | 1632.73 | 1611.39 | 1613.78 | 19.4140 | 83.1221 |

| 2021-10-29 | 1624.31 | 1627.01 | 1629.25 | 1619.14 | 1623.43 | 19.5307 | 83.1111 |

| 2021-10-28 | 1627.61 | 1626.27 | 1632.30 | 1622.56 | 1624.31 | 19.5438 | 83.6187 |

| … | … | … | … | … | … | … | … |

| NaT | NaN | NaN | NaN | NaN | NaN | NaN | 54.6940 |

| NaT | NaN | NaN | NaN | NaN | NaN | NaN | 54.6926 |

| NaT | NaN | NaN | NaN | NaN | NaN | NaN | 54.6938 |

| NaT | NaN | NaN | NaN | NaN | NaN | NaN | 54.6979 |

| NaT | NaN | NaN | NaN | NaN | NaN | NaN | 54.6952 |

3088 rows × 7 columns

data_gdpq| GDP | |

|---|---|

| Date | |

| 2016-03-31 | 3597737000000 |

| 2016-06-30 | 3557050000000 |

| 2016-09-30 | 3628315000000 |

| 2016-12-31 | 3807235000000 |

| 2017-03-31 | 3830606000000 |

| 2017-06-30 | 3753348000000 |

| 2017-09-30 | 3854593000000 |

| 2017-12-31 | 4050117000000 |

| 2018-03-31 | 4051915000000 |

| 2018-06-30 | 3998560000000 |

| 2018-09-30 | 4063764000000 |

| 2018-12-31 | 4254466000000 |

| 2019-03-31 | 4223706000000 |

| 2019-06-30 | 4156001000000 |

| 2019-09-30 | 4181774000000 |

| 2019-12-31 | 4336605000000 |

| 2020-03-31 | 4158483000000 |

| 2020-06-30 | 3545622000000 |

| 2020-09-30 | 3860959000000 |

| 2020-12-31 | 4133222000000 |

| 2021-03-31 | 4070526000000 |

| 2021-06-30 | 3923731000000 |

1422 rows × 7 columns

Merging DataFrames

We will now merge the data between data_set and data_set_eps DataFrames:

min_date = data_set_eps.index.min()

max_date = data_set_eps.index.max()

date_range = (min_date, max_date)date_range

(Timestamp('2016-01-04 00:00:00'), Timestamp('2021-11-03 00:00:00'))data_set_eps_subset = data_set_eps.loc[data_set.index, ["PE", "EPS"]]

df1 = pd.merge(data_set, data_set_eps_subset, how="left", left_index=True, right_index=True)data_set_eps_subset| PE | EPS | |

|---|---|---|

| Date | ||

| 2016-01-04 | 17.3305 | 72.2368 |

| 2016-01-05 | 17.1919 | 72.2431 |

| 2016-01-06 | 17.2866 | 72.2438 |

| 2016-01-07 | 16.8012 | 72.2363 |

| 2016-01-08 | 17.0010 | 72.2296 |

| … | … | … |

| 2021-10-28 | 19.5438 | 83.6187 |

| 2021-10-29 | 19.5307 | 83.1111 |

| 2021-11-01 | 19.4140 | 83.1221 |

| 2021-11-02 | 19.4637 | 83.1246 |

| 2021-11-03 | 19.3909 | 83.1235 |

1422 rows × 2 columns

df1| Prior | Open | High | Low | Close | PE_x | PE_y | EPS | |

|---|---|---|---|---|---|---|---|---|

| Date | ||||||||

| 2016-01-04 | 1288.02 | 1286.29 | 1286.36 | 1260.96 | 1263.41 | 22.12 | 17.3305 | 72.2368 |

| 2016-01-05 | 1263.41 | 1267.20 | 1270.07 | 1251.87 | 1253.34 | 21.99 | 17.1919 | 72.2431 |

| 2016-01-06 | 1253.34 | 1249.82 | 1260.88 | 1247.89 | 1260.04 | 22.10 | 17.2866 | 72.2438 |

| 2016-01-07 | 1260.04 | 1237.81 | 1244.04 | 1224.83 | 1224.83 | 21.46 | 16.8012 | 72.2363 |

| 2016-01-08 | 1224.83 | 1232.31 | 1246.70 | 1228.18 | 1244.18 | 21.81 | 17.0010 | 72.2296 |

| … | … | … | … | … | … | … | … | … |

| 2021-10-28 | 1627.61 | 1626.27 | 1632.30 | 1622.56 | 1624.31 | 20.81 | 19.5438 | 83.6187 |

| 2021-10-29 | 1624.31 | 1627.01 | 1629.25 | 1619.14 | 1623.43 | 21.02 | 19.5307 | 83.1111 |

| 2021-11-01 | 1623.43 | 1627.54 | 1632.73 | 1611.39 | 1613.78 | 20.89 | 19.4140 | 83.1221 |

| 2021-11-02 | 1613.78 | 1616.86 | 1621.69 | 1608.64 | 1617.89 | 20.96 | 19.4637 | 83.1246 |

| 2021-11-03 | 1617.89 | 1620.90 | 1623.08 | 1607.72 | 1611.92 | 20.87 | 19.3909 | 83.1235 |

1422 rows × 8 columns

Adding GDP Data to the Merged DataFrame

Next, we will add the GDP data to the merged DataFrame

data_gdpq.index.year

Int64Index([2016, 2016, 2016, 2016, 2017, 2017, 2017, 2017, 2018, 2018, 2018,2018, 2019, 2019, 2019, 2019, 2020, 2020, 2020, 2020, 2021, 2021],

dtype='int64', name='Date')data_gdpq.groupby(data_gdpq.index.year)['GDP'].mean()

Date

2016 3.647584e+12

2017 3.872166e+12

2018 4.092176e+12

2019 4.224522e+12

2020 3.924572e+12

2021 3.997128e+12

Name: GDP, dtype: float64gdp_yearly = data_gdpq.groupby(data_gdpq.index.year)['GDP'].mean()

for i in range(2016,2022):

df1.loc[str(i),'gdp'] = gdp_yearly.loc[i]df1| Prior | Open | High | Low | Close | PE_x | PE_y | EPS | gdp | |

|---|---|---|---|---|---|---|---|---|---|

| Date | |||||||||

| 2016-01-04 | 1288.02 | 1286.29 | 1286.36 | 1260.96 | 1263.41 | 22.12 | 17.3305 | 72.2368 | 3.647584e+12 |

| 2016-01-05 | 1263.41 | 1267.20 | 1270.07 | 1251.87 | 1253.34 | 21.99 | 17.1919 | 72.2431 | 3.647584e+12 |

| 2016-01-06 | 1253.34 | 1249.82 | 1260.88 | 1247.89 | 1260.04 | 22.10 | 17.2866 | 72.2438 | 3.647584e+12 |

| 2016-01-07 | 1260.04 | 1237.81 | 1244.04 | 1224.83 | 1224.83 | 21.46 | 16.8012 | 72.2363 | 3.647584e+12 |

| 2016-01-08 | 1224.83 | 1232.31 | 1246.70 | 1228.18 | 1244.18 | 21.81 | 17.0010 | 72.2296 | 3.647584e+12 |

| … | … | … | … | … | … | … | … | … | … |

| 2021-10-28 | 1627.61 | 1626.27 | 1632.30 | 1622.56 | 1624.31 | 20.81 | 19.5438 | 83.6187 | 3.997128e+12 |

| 2021-10-29 | 1624.31 | 1627.01 | 1629.25 | 1619.14 | 1623.43 | 21.02 | 19.5307 | 83.1111 | 3.997128e+12 |

| 2021-11-01 | 1623.43 | 1627.54 | 1632.73 | 1611.39 | 1613.78 | 20.89 | 19.4140 | 83.1221 | 3.997128e+12 |

| 2021-11-02 | 1613.78 | 1616.86 | 1621.69 | 1608.64 | 1617.89 | 20.96 | 19.4637 | 83.1246 | 3.997128e+12 |

| 2021-11-03 | 1617.89 | 1620.90 | 1623.08 | 1607.72 | 1611.92 | 20.87 | 19.3909 | 83.1235 | 3.997128e+12 |

1422 rows × 9 columns

Calculating and Adding Stock Return to the DataFrame

We will now calculate the daily stock return and add it to the DataFrame

df1['Return_shift'] = df1.Close.pct_change()df1.dropna(inplace=True)df1| Prior | Open | High | Low | Close | PE_x | PE_y | EPS | gdp | Return_shift | |

|---|---|---|---|---|---|---|---|---|---|---|

| Date | ||||||||||

| 2016-01-05 | 1263.41 | 1267.20 | 1270.07 | 1251.87 | 1253.34 | 21.99 | 17.1919 | 72.2431 | 3.647584e+12 | -0.007970 |

| 2016-01-06 | 1253.34 | 1249.82 | 1260.88 | 1247.89 | 1260.04 | 22.10 | 17.2866 | 72.2438 | 3.647584e+12 | 0.005346 |

| 2016-01-07 | 1260.04 | 1237.81 | 1244.04 | 1224.83 | 1224.83 | 21.46 | 16.8012 | 72.2363 | 3.647584e+12 | -0.027944 |

| 2016-01-08 | 1224.83 | 1232.31 | 1246.70 | 1228.18 | 1244.18 | 21.81 | 17.0010 | 72.2296 | 3.647584e+12 | 0.015798 |

| 2016-01-11 | 1244.18 | 1233.80 | 1235.18 | 1220.96 | 1234.50 | 21.63 | 16.8695 | 72.2242 | 3.647584e+12 | -0.007780 |

| … | … | … | … | … | … | … | … | … | … | … |

| 2021-10-28 | 1627.61 | 1626.27 | 1632.30 | 1622.56 | 1624.31 | 20.81 | 19.5438 | 83.6187 | 3.997128e+12 | -0.002028 |

| 2021-10-29 | 1624.31 | 1627.01 | 1629.25 | 1619.14 | 1623.43 | 21.02 | 19.5307 | 83.1111 | 3.997128e+12 | -0.000542 |

| 2021-11-01 | 1623.43 | 1627.54 | 1632.73 | 1611.39 | 1613.78 | 20.89 | 19.4140 | 83.1221 | 3.997128e+12 | -0.005944 |

| 2021-11-02 | 1613.78 | 1616.86 | 1621.69 | 1608.64 | 1617.89 | 20.96 | 19.4637 | 83.1246 | 3.997128e+12 | 0.002547 |

| 2021-11-03 | 1617.89 | 1620.90 | 1623.08 | 1607.72 | 1611.92 | 20.87 | 19.3909 | 83.1235 | 3.997128e+12 | -0.003690 |

1421 rows × 10 columns

df1.loc[(df1.EPS>70)& (df1.EPS<80)]| Prior | Open | High | Low | Close | PE_x | PE_y | EPS | gdp | Return_shift | PE_Label | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Date | |||||||||||

| 2016-01-05 | 1263.41 | 1267.20 | 1270.07 | 1251.87 | 1253.34 | 21.99 | 17.1919 | 72.2431 | 3.647584e+12 | -0.007970 | 1 |

| 2016-01-06 | 1253.34 | 1249.82 | 1260.88 | 1247.89 | 1260.04 | 22.10 | 17.2866 | 72.2438 | 3.647584e+12 | 0.005346 | 1 |

| 2016-01-07 | 1260.04 | 1237.81 | 1244.04 | 1224.83 | 1224.83 | 21.46 | 16.8012 | 72.2363 | 3.647584e+12 | -0.027944 | 1 |

| 2016-01-08 | 1224.83 | 1232.31 | 1246.70 | 1228.18 | 1244.18 | 21.81 | 17.0010 | 72.2296 | 3.647584e+12 | 0.015798 | 1 |

| 2016-01-11 | 1244.18 | 1233.80 | 1235.18 | 1220.96 | 1234.50 | 21.63 | 16.8695 | 72.2242 | 3.647584e+12 | -0.007780 | 1 |

| … | … | … | … | … | … | … | … | … | … | … | … |

| 2016-05-18 | 1406.57 | 1407.66 | 1410.04 | 1399.36 | 1400.50 | 21.16 | 19.3878 | 74.2615 | 3.647584e+12 | -0.004315 | 1 |

| 2016-05-19 | 1400.50 | 1399.39 | 1400.97 | 1384.12 | 1385.86 | 20.94 | 19.1851 | 74.2568 | 3.647584e+12 | -0.010453 | 1 |

| 2016-05-23 | 1385.86 | 1387.81 | 1388.88 | 1377.65 | 1381.69 | 20.88 | 19.1272 | 74.2602 | 3.647584e+12 | -0.003009 | 1 |

| 2016-05-24 | 1381.69 | 1381.54 | 1386.15 | 1376.74 | 1384.26 | 20.92 | 19.1611 | 74.2644 | 3.647584e+12 | 0.001860 | 1 |

| 2016-05-25 | 1384.26 | 1394.65 | 1398.35 | 1390.19 | 1397.63 | 21.13 | 19.3460 | 74.3830 | 3.647584e+12 | 0.009659 | 1 |

93 rows × 11 columns

df1.loc[ (df1.EPS>35)&(df1.EPS<40)]| Prior | Open | High | Low | Close | PE_x | PE_y | EPS | gdp | Return_shift | PE_Label | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Date | |||||||||||

| 2020-12-03 | 1417.95 | 1424.31 | 1439.22 | 1420.69 | 1438.32 | 28.49 | 26.2152 | 38.9297 | 3.924572e+12 | 0.014366 | 2 |

| 2020-12-04 | 1438.32 | 1439.14 | 1454.94 | 1439.14 | 1449.83 | 28.73 | 26.4263 | 38.9327 | 3.924572e+12 | 0.008002 | 2 |

| 2020-12-08 | 1449.83 | 1447.71 | 1484.73 | 1442.65 | 1478.92 | 29.34 | 26.9521 | 38.9373 | 3.924572e+12 | 0.020064 | 2 |

| 2020-12-09 | 1478.92 | 1491.67 | 1503.89 | 1474.83 | 1482.67 | 29.41 | 27.0420 | 38.9369 | 3.924572e+12 | 0.002536 | 2 |

| 2020-12-14 | 1482.67 | 1490.79 | 1495.18 | 1471.56 | 1476.13 | 29.28 | 26.9259 | 38.9370 | 3.924572e+12 | -0.004411 | 2 |

| … | … | … | … | … | … | … | … | … | … | … | … |

| 2021-03-05 | 1534.11 | 1530.05 | 1553.92 | 1529.83 | 1544.11 | 40.32 | 39.5819 | 39.0209 | 3.997128e+12 | 0.006518 | 6 |

| 2021-03-08 | 1544.11 | 1558.79 | 1562.56 | 1540.64 | 1543.76 | 40.29 | 39.5730 | 39.0214 | 3.997128e+12 | -0.000227 | 6 |

| 2021-03-09 | 1543.76 | 1551.57 | 1554.96 | 1537.23 | 1550.59 | 40.44 | 39.7479 | 39.0213 | 3.997128e+12 | 0.004424 | 6 |

| 2021-03-10 | 1550.59 | 1553.23 | 1573.55 | 1550.45 | 1573.05 | 41.00 | 40.3238 | 39.0213 | 3.997128e+12 | 0.014485 | 6 |

| 2021-03-11 | 1573.05 | 1583.13 | 1584.61 | 1569.87 | 1575.13 | 41.07 | 40.3772 | 39.0857 | 3.997128e+12 | 0.001322 | 6 |

64 rows × 11 columns

df1.loc[ (df1.EPS>100)]| Prior | Open | High | Low | Close | PE_x | PE_y | EPS | gdp | Return_shift | PE_Label | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Date | |||||||||||

| 2018-04-02 | 1776.26 | 1775.24 | 1783.73 | 1771.58 | 1782.28 | 18.35 | 17.9799 | 101.0242 | 4.092176e+12 | 0.003389 | 1 |

| 2018-04-03 | 1782.28 | 1774.45 | 1779.04 | 1764.18 | 1765.24 | 18.17 | 17.8016 | 101.0231 | 4.092176e+12 | -0.009561 | 1 |

| 2018-04-04 | 1765.24 | 1766.67 | 1771.58 | 1724.90 | 1724.98 | 17.75 | 17.3944 | 101.0234 | 4.092176e+12 | -0.022807 | 1 |

| 2018-04-05 | 1724.98 | 1735.58 | 1740.84 | 1724.88 | 1739.92 | 17.90 | 17.5470 | 101.0272 | 4.092176e+12 | 0.008661 | 1 |

| 2018-04-09 | 1739.92 | 1736.54 | 1752.91 | 1735.38 | 1751.27 | 18.03 | 17.6620 | 101.0266 | 4.092176e+12 | 0.006523 | 1 |

| … | … | … | … | … | … | … | … | … | … | … | … |

| 2018-08-10 | 1722.48 | 1718.40 | 1719.03 | 1705.20 | 1705.96 | 17.32 | 16.9411 | 105.4328 | 4.092176e+12 | -0.009591 | 1 |

| 2018-08-21 | 1701.42 | 1703.79 | 1707.63 | 1688.59 | 1694.63 | 16.83 | 16.8285 | 100.6324 | 4.092176e+12 | -0.003991 | 1 |

| 2018-08-22 | 1694.63 | 1696.96 | 1705.91 | 1695.34 | 1698.30 | 16.89 | 16.8666 | 100.6112 | 4.092176e+12 | 0.002166 | 1 |

| 2018-10-09 | 1696.22 | 1700.55 | 1708.72 | 1690.92 | 1696.92 | 16.73 | 16.0854 | 105.4485 | 4.092176e+12 | 0.000413 | 1 |

| 2018-10-10 | 1696.92 | 1709.19 | 1721.82 | 1707.63 | 1721.82 | 16.98 | 16.3222 | 105.4503 | 4.092176e+12 | 0.014674 | 1 |

92 rows × 11 columns

Create label for ML training

def pe(pe):

if pe <=20:

return 1

elif (pe>20)&(pe<=28):

return 2

elif (pe>28)&(pe<=30):

return 3

elif (pe > 30) & (pe <= 34):

return 4

elif (pe > 34) & (pe <= 38):

return 5

elif (pe > 38) & (pe <= 42):

return 6

elif pe > 42:

return 7def eps(eps):

if eps <=40:

return 1

elif (eps>40)&(eps<=50):

return 2

elif (eps>50)&(eps<=60):

return 3

elif (eps > 60) & (eps <= 70):

return 4

elif (eps > 70) & (eps <= 80):

return 5

elif (eps > 80) & (eps <= 90):

return 6

elif (eps > 90) & (eps <= 100):

return 7

elif eps > 100 :

return 8def gdp(gdp):

if gdp <=3.750000e+12:

return 1

elif (gdp>3.750000e+12)&(gdp<=4.000000e+12):

return 2

elif (gdp>4.000000e+12)&(gdp<=4.250000e+12):

return 3

elif eps > 4.250000e+12 :

return 4

df1['PE_Label'] = df1['PE_y'].apply(pe)df1['EPS_Label'] = df1['EPS'].apply(eps)df1['GDP_Label'] = df1['gdp'].apply(gdp)df1| Prior | Open | High | Low | Close | PE_x | PE_y | EPS | gdp | Return_shift | PE_Label | EPS_Label | GDP_Label | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Date | |||||||||||||

| 2016-01-05 | 1263.41 | 1267.20 | 1270.07 | 1251.87 | 1253.34 | 21.99 | 17.1919 | 72.2431 | 3.647584e+12 | -0.007970 | 1 | 5 | 1 |

| 2016-01-06 | 1253.34 | 1249.82 | 1260.88 | 1247.89 | 1260.04 | 22.10 | 17.2866 | 72.2438 | 3.647584e+12 | 0.005346 | 1 | 5 | 1 |

| 2016-01-07 | 1260.04 | 1237.81 | 1244.04 | 1224.83 | 1224.83 | 21.46 | 16.8012 | 72.2363 | 3.647584e+12 | -0.027944 | 1 | 5 | 1 |

| 2016-01-08 | 1224.83 | 1232.31 | 1246.70 | 1228.18 | 1244.18 | 21.81 | 17.0010 | 72.2296 | 3.647584e+12 | 0.015798 | 1 | 5 | 1 |

| 2016-01-11 | 1244.18 | 1233.80 | 1235.18 | 1220.96 | 1234.50 | 21.63 | 16.8695 | 72.2242 | 3.647584e+12 | -0.007780 | 1 | 5 | 1 |

| … | … | … | … | … | … | … | … | … | … | … | … | … | … |

| 2021-10-28 | 1627.61 | 1626.27 | 1632.30 | 1622.56 | 1624.31 | 20.81 | 19.5438 | 83.6187 | 3.997128e+12 | -0.002028 | 1 | 6 | 2 |

| 2021-10-29 | 1624.31 | 1627.01 | 1629.25 | 1619.14 | 1623.43 | 21.02 | 19.5307 | 83.1111 | 3.997128e+12 | -0.000542 | 1 | 6 | 2 |

| 2021-11-01 | 1623.43 | 1627.54 | 1632.73 | 1611.39 | 1613.78 | 20.89 | 19.4140 | 83.1221 | 3.997128e+12 | -0.005944 | 1 | 6 | 2 |

| 2021-11-02 | 1613.78 | 1616.86 | 1621.69 | 1608.64 | 1617.89 | 20.96 | 19.4637 | 83.1246 | 3.997128e+12 | 0.002547 | 1 | 6 | 2 |

| 2021-11-03 | 1617.89 | 1620.90 | 1623.08 | 1607.72 | 1611.92 | 20.87 | 19.3909 | 83.1235 | 3.997128e+12 | -0.003690 | 1 | 6 | 2 |

1421 rows × 13 columns

Data Preparation:

First, we need to split our dataset into training and testing sets. The training set will be used to train our model, while the testing set will be used to evaluate its performance.

X = df1[['EPS','PE_y','gdp','EPS_Label', 'PE_Label','GDP_Label']]

y = df1['Return_shift']X_train = X.iloc[:1000]

y_train = y.iloc[:1000]

X_test = X.iloc[1000:1200]

y_test = y.iloc[1000:1200]X_train| EPS | PE_y | gdp | EPS_Label | PE_Label | GDP_Label | |

|---|---|---|---|---|---|---|

| Date | ||||||

| 2016-01-05 | 72.2431 | 17.1919 | 3.647584e+12 | 5 | 1 | 1 |

| 2016-01-06 | 72.2438 | 17.2866 | 3.647584e+12 | 5 | 1 | 1 |

| 2016-01-07 | 72.2363 | 16.8012 | 3.647584e+12 | 5 | 1 | 1 |

| 2016-01-08 | 72.2296 | 17.0010 | 3.647584e+12 | 5 | 1 | 1 |

| 2016-01-11 | 72.2242 | 16.8695 | 3.647584e+12 | 5 | 1 | 1 |

| … | … | … | … | … | … | … |

| 2020-01-29 | 87.4341 | 17.4639 | 3.924572e+12 | 6 | 1 | 2 |

| 2020-01-30 | 87.4127 | 17.4568 | 3.924572e+12 | 6 | 1 | 2 |

| 2020-01-31 | 87.4291 | 17.3440 | 3.924572e+12 | 6 | 1 | 2 |

| 2020-02-03 | 87.3809 | 17.1378 | 3.924572e+12 | 6 | 1 | 2 |

| 2020-02-04 | 87.3742 | 17.4058 | 3.924572e+12 | 6 | 1 | 2 |

1000 rows × 6 columns

y_train

Date

2016-01-05 -0.007970

2016-01-06 0.005346

2016-01-07 -0.027944

2016-01-08 0.015798

2016-01-11 -0.007780

...

2020-01-29 0.007487

2020-01-30 -0.000394

2020-01-31 -0.006463

2020-02-03 -0.011941

2020-02-04 0.015588

Name: Return_shift, Length: 1000, dtype: float64X_test| EPS | PE_y | gdp | EPS_Label | PE_Label | GDP_Label | |

|---|---|---|---|---|---|---|

| Date | ||||||

| 2020-02-05 | 87.3689 | 17.5751 | 3.924572e+12 | 6 | 1 | 2 |

| 2020-02-06 | 87.3775 | 17.5939 | 3.924572e+12 | 6 | 1 | 2 |

| 2020-02-07 | 87.3785 | 17.5876 | 3.924572e+12 | 6 | 1 | 2 |

| 2020-02-11 | 87.3733 | 17.4579 | 3.924572e+12 | 6 | 1 | 2 |

| 2020-02-12 | 87.3735 | 17.6405 | 3.924572e+12 | 6 | 1 | 2 |

| … | … | … | … | … | … | … |

| 2020-11-24 | 54.8500 | 25.5605 | 3.924572e+12 | 3 | 2 | 2 |

| 2020-11-25 | 54.8633 | 25.8183 | 3.924572e+12 | 3 | 2 | 2 |

| 2020-11-26 | 55.5504 | 26.1422 | 3.924572e+12 | 3 | 2 | 2 |

| 2020-11-27 | 55.4210 | 26.2192 | 3.924572e+12 | 3 | 2 | 2 |

| 2020-11-30 | 55.4316 | 25.6753 | 3.924572e+12 | 3 | 2 | 2 |

200 rows × 6 columns

Model Training and Evaluation:

Now that we have prepared our data, we can start building the linear regression model.

We will use the Scikit-learn library to create and train our model,

and then evaluate its performance using various metrics such as R-squared,

Mean Absolute Error (MAE), Mean Squared Error (MSE), and Root Mean Squared Error (RMSE).

from sklearn.model_selection import train_test_split

from sklearn.linear_model import LinearRegression

from sklearn import metrics

from sklearn.model_selection import cross_val_score

model = LinearRegression()

model.fit(X_train, y_train)

y_pred = model.predict(X_test)

print('Score = ', metrics.r2_score(y_test,y_pred))

m = model.coef_

print("coef = ",m)

b = model.intercept_

print("intercept = ",b)

print("MAE = ", metrics.mean_absolute_error(y_test,y_pred))

print("MSE = ", metrics.mean_squared_error(y_test,y_pred))

print("RMSE = ", np.sqrt(metrics.mean_squared_error(y_test,y_pred)))

Score = 0.016679949410685402

coef = [ 4.68128493e-05 4.35681735e-04 3.02324355e-15 2.79260864e-05

-1.35296661e-03 -1.46159773e-03]

intercept = -0.019300039650165336

MAE = 0.012205326313264547

MSE = 0.0003814982502499546

RMSE = 0.01953198019274939Create report

df_report = pd.DataFrame({'Actual': y_test, 'Predict':y_pred})

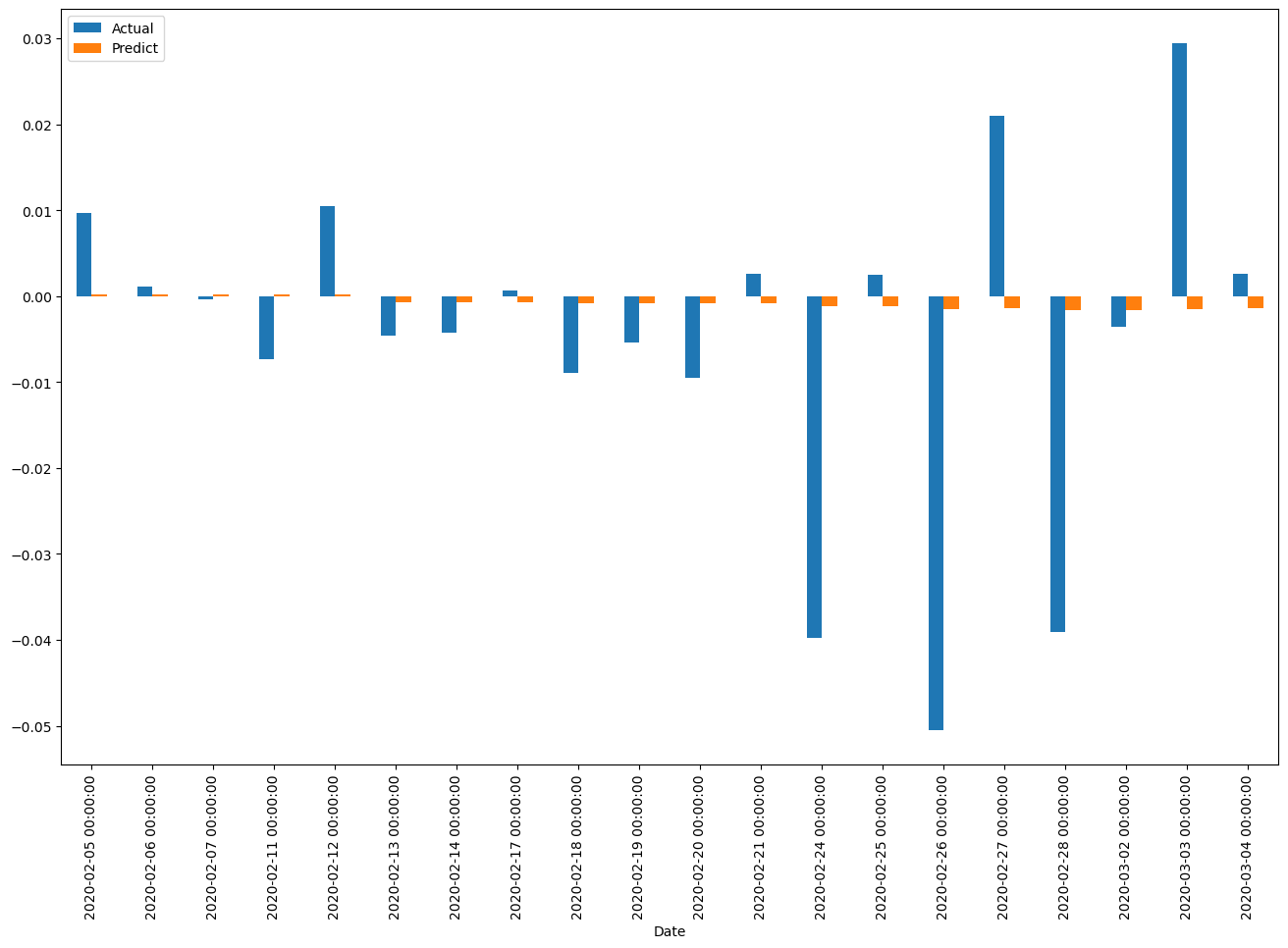

df_report| Actual | Predict | |

|---|---|---|

| Date | ||

| 2020-02-05 | 0.009714 | 0.000203 |

| 2020-02-06 | 0.001076 | 0.000212 |

| 2020-02-07 | -0.000358 | 0.000209 |

| 2020-02-11 | -0.007367 | 0.000153 |

| 2020-02-12 | 0.010440 | 0.000232 |

| … | … | … |

| 2020-11-24 | -0.013235 | 0.000723 |

| 2020-11-25 | 0.010053 | 0.000836 |

| 2020-11-26 | 0.012601 | 0.001010 |

| 2020-11-27 | 0.002944 | 0.001037 |

| 2020-11-30 | -0.020497 | 0.000801 |

200 rows × 2 columns

df_report_example = df_report.head(20)

df_report_example.plot(kind='bar',figsize=(16,10))

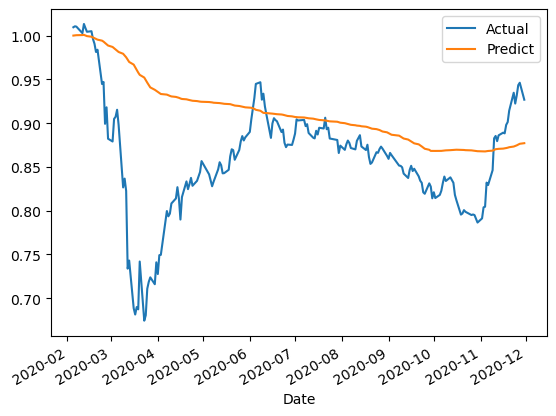

(df_report+1).cumprod().plot()

test model with data split

X_live = df1.iloc[1200:]X_live| Prior | Open | High | Low | Close | PE_x | PE_y | EPS | gdp | Return_shift | PE_Label | EPS_Label | GDP_Label | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Date | |||||||||||||

| 2020-12-01 | 1408.31 | 1419.28 | 1430.03 | 1416.39 | 1420.87 | 28.11 | 25.9028 | 55.4349 | 3.924572e+12 | 0.008918 | 2 | 3 | 2 |

| 2020-12-02 | 1420.87 | 1416.46 | 1430.49 | 1415.10 | 1417.95 | 28.06 | 25.8395 | 55.3846 | 3.924572e+12 | -0.002055 | 2 | 3 | 2 |

| 2020-12-03 | 1417.95 | 1424.31 | 1439.22 | 1420.69 | 1438.32 | 28.49 | 26.2152 | 38.9297 | 3.924572e+12 | 0.014366 | 2 | 1 | 2 |

| 2020-12-04 | 1438.32 | 1439.14 | 1454.94 | 1439.14 | 1449.83 | 28.73 | 26.4263 | 38.9327 | 3.924572e+12 | 0.008002 | 2 | 1 | 2 |

| 2020-12-08 | 1449.83 | 1447.71 | 1484.73 | 1442.65 | 1478.92 | 29.34 | 26.9521 | 38.9373 | 3.924572e+12 | 0.020064 | 2 | 1 | 2 |

| … | … | … | … | … | … | … | … | … | … | … | … | … | … |

| 2021-10-28 | 1627.61 | 1626.27 | 1632.30 | 1622.56 | 1624.31 | 20.81 | 19.5438 | 83.6187 | 3.997128e+12 | -0.002028 | 1 | 6 | 2 |

| 2021-10-29 | 1624.31 | 1627.01 | 1629.25 | 1619.14 | 1623.43 | 21.02 | 19.5307 | 83.1111 | 3.997128e+12 | -0.000542 | 1 | 6 | 2 |

| 2021-11-01 | 1623.43 | 1627.54 | 1632.73 | 1611.39 | 1613.78 | 20.89 | 19.4140 | 83.1221 | 3.997128e+12 | -0.005944 | 1 | 6 | 2 |

| 2021-11-02 | 1613.78 | 1616.86 | 1621.69 | 1608.64 | 1617.89 | 20.96 | 19.4637 | 83.1246 | 3.997128e+12 | 0.002547 | 1 | 6 | 2 |

| 2021-11-03 | 1617.89 | 1620.90 | 1623.08 | 1607.72 | 1611.92 | 20.87 | 19.3909 | 83.1235 | 3.997128e+12 | -0.003690 | 1 | 6 | 2 |

221 rows × 13 columns

X_live[['EPS','PE_y','gdp','EPS_Label', 'PE_Label','GDP_Label']]| EPS | PE_y | gdp | EPS_Label | PE_Label | GDP_Label | |

|---|---|---|---|---|---|---|

| Date | ||||||

| 2020-12-01 | 55.4349 | 25.9028 | 3.924572e+12 | 3 | 2 | 2 |

| 2020-12-02 | 55.3846 | 25.8395 | 3.924572e+12 | 3 | 2 | 2 |

| 2020-12-03 | 38.9297 | 26.2152 | 3.924572e+12 | 1 | 2 | 2 |

| 2020-12-04 | 38.9327 | 26.4263 | 3.924572e+12 | 1 | 2 | 2 |

| 2020-12-08 | 38.9373 | 26.9521 | 3.924572e+12 | 1 | 2 | 2 |

| … | … | … | … | … | … | … |

| 2021-10-28 | 83.6187 | 19.5438 | 3.997128e+12 | 6 | 1 | 2 |

| 2021-10-29 | 83.1111 | 19.5307 | 3.997128e+12 | 6 | 1 | 2 |

| 2021-11-01 | 83.1221 | 19.4140 | 3.997128e+12 | 6 | 1 | 2 |

| 2021-11-02 | 83.1246 | 19.4637 | 3.997128e+12 | 6 | 1 | 2 |

| 2021-11-03 | 83.1235 | 19.3909 | 3.997128e+12 | 6 | 1 | 2 |

221 rows × 6 columns

X_live| Prior | Open | High | Low | Close | PE_x | PE_y | EPS | gdp | Return_shift | PE_Label | EPS_Label | GDP_Label | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Date | |||||||||||||

| 2020-12-01 | 1408.31 | 1419.28 | 1430.03 | 1416.39 | 1420.87 | 28.11 | 25.9028 | 55.4349 | 3.924572e+12 | 0.008918 | 2 | 3 | 2 |

| 2020-12-02 | 1420.87 | 1416.46 | 1430.49 | 1415.10 | 1417.95 | 28.06 | 25.8395 | 55.3846 | 3.924572e+12 | -0.002055 | 2 | 3 | 2 |

| 2020-12-03 | 1417.95 | 1424.31 | 1439.22 | 1420.69 | 1438.32 | 28.49 | 26.2152 | 38.9297 | 3.924572e+12 | 0.014366 | 2 | 1 | 2 |

| 2020-12-04 | 1438.32 | 1439.14 | 1454.94 | 1439.14 | 1449.83 | 28.73 | 26.4263 | 38.9327 | 3.924572e+12 | 0.008002 | 2 | 1 | 2 |

| 2020-12-08 | 1449.83 | 1447.71 | 1484.73 | 1442.65 | 1478.92 | 29.34 | 26.9521 | 38.9373 | 3.924572e+12 | 0.020064 | 2 | 1 | 2 |

| … | … | … | … | … | … | … | … | … | … | … | … | … | … |

| 2021-10-28 | 1627.61 | 1626.27 | 1632.30 | 1622.56 | 1624.31 | 20.81 | 19.5438 | 83.6187 | 3.997128e+12 | -0.002028 | 1 | 6 | 2 |

| 2021-10-29 | 1624.31 | 1627.01 | 1629.25 | 1619.14 | 1623.43 | 21.02 | 19.5307 | 83.1111 | 3.997128e+12 | -0.000542 | 1 | 6 | 2 |

| 2021-11-01 | 1623.43 | 1627.54 | 1632.73 | 1611.39 | 1613.78 | 20.89 | 19.4140 | 83.1221 | 3.997128e+12 | -0.005944 | 1 | 6 | 2 |

| 2021-11-02 | 1613.78 | 1616.86 | 1621.69 | 1608.64 | 1617.89 | 20.96 | 19.4637 | 83.1246 | 3.997128e+12 | 0.002547 | 1 | 6 | 2 |

| 2021-11-03 | 1617.89 | 1620.90 | 1623.08 | 1607.72 | 1611.92 | 20.87 | 19.3909 | 83.1235 | 3.997128e+12 | -0.003690 | 1 | 6 | 2 |

221 rows × 13 columns

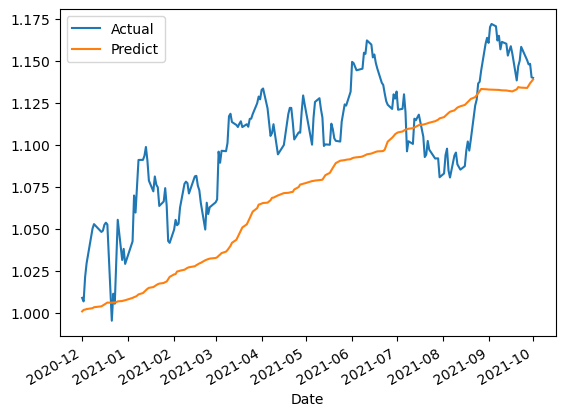

live_data =X_live[['EPS','PE_y','gdp','EPS_Label', 'PE_Label','GDP_Label']]live_data['Return_shift']=model.predict(live_data)df_live_report = pd.DataFrame({'Actual': X_live['Return_shift'], 'Predict':live_data['Return_shift']})

df_live_report| Actual | Predict | |

|---|---|---|

| Date | ||

| 2020-12-01 | 0.008918 | 0.000900 |

| 2020-12-02 | -0.002055 | 0.000870 |

| 2020-12-03 | 0.014366 | 0.000208 |

| 2020-12-04 | 0.008002 | 0.000300 |

| 2020-12-08 | 0.020064 | 0.000529 |

| … | … | … |

| 2021-10-28 | -0.002028 | 0.001105 |

| 2021-10-29 | -0.000542 | 0.001075 |

| 2021-11-01 | -0.005944 | 0.001025 |

| 2021-11-02 | 0.002547 | 0.001047 |

| 2021-11-03 | -0.003690 | 0.001015 |

221 rows × 2 columns

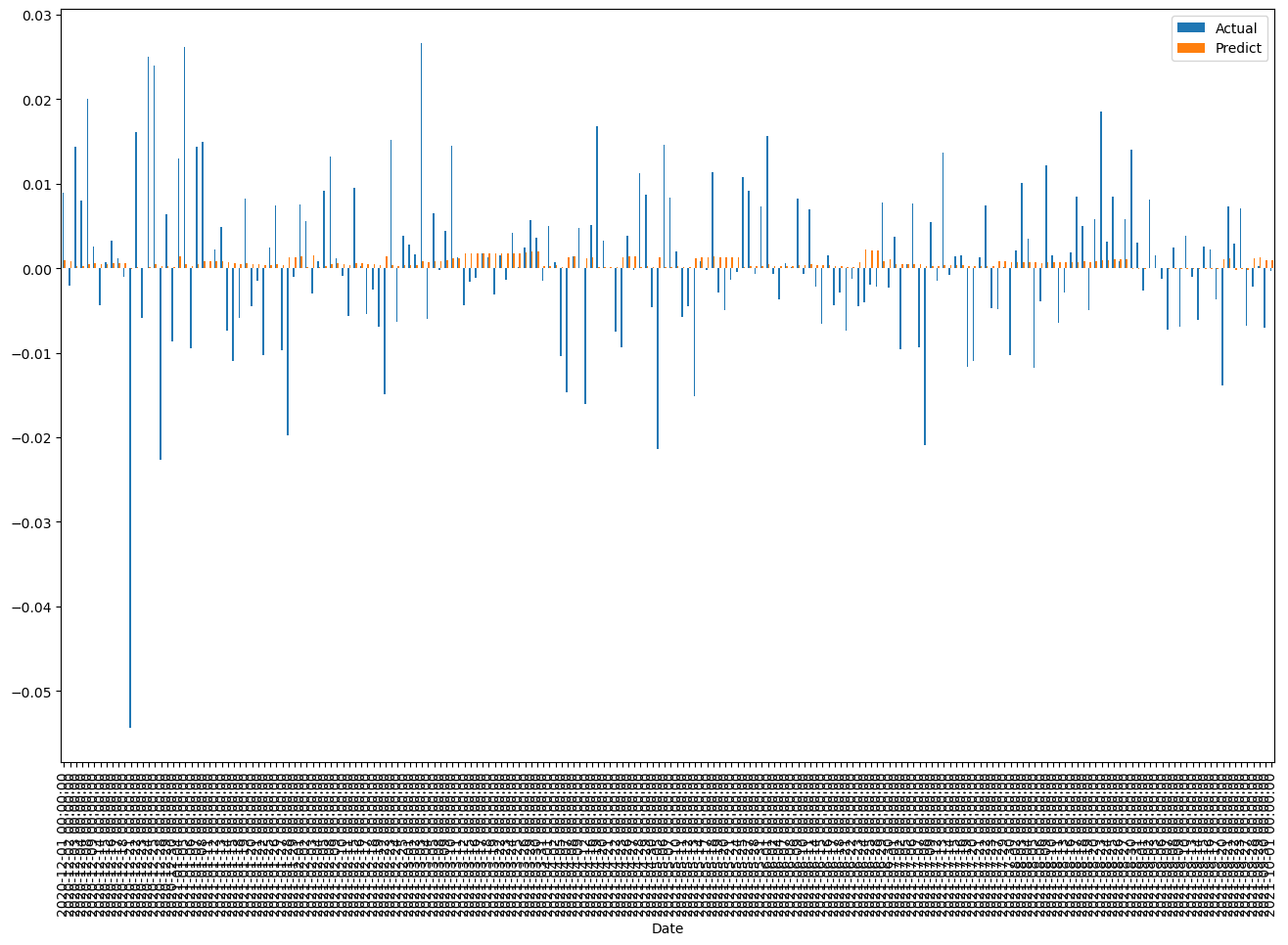

df_live_report_exmaple = df_live_report.head(200)

df_live_report_exmaple.plot(kind='bar',figsize=(16,10))

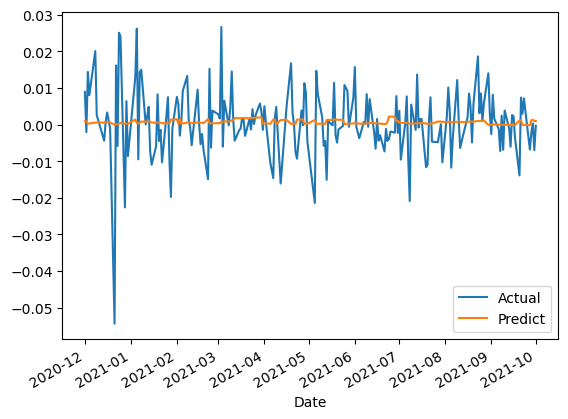

(df_live_report_exmaple).plot()

(df_live_report_exmaple+1).cumprod().plot()

Conclusion

In this article, we demonstrated how to perform stock analysis and predict stock returns using Python. We started by importing and merging multiple datasets,

including historical stock prices, earnings per share (EPS), and GDP data. After merging the datasets and adding stock return calculations, we used linear regression to predict stock returns based on historical data.

We then visualized the results using various libraries like pandas, matplotlib, numpy, and seaborn.

The results showed that our linear regression model provided a reasonable prediction of stock returns, although it is important to note that stock market predictions are inherently uncertain and should not be solely relied upon for investment decisions.

Further improvements to the model could be achieved by incorporating additional variables, using more advanced techniques, or incorporating domain-specific knowledge.

Overall, this article serves as a foundation for further exploration into stock analysis and prediction using Python, providing valuable insights for investors and analysts looking to harness the power of data-driven decision-making.