What Idea about Correlation Currency ?

The idea of correlation-based currency pair trading is to analyze the correlation between different currency pairs and utilize this information to make informed trading decisions. By identifying currency pairs with positive correlation, we can implement pair trading strategies or predict the potential movement of one currency based on the performance of another. In this example, we will analyze the correlation between the following currency pairs:

| Currency Pair |

|---|

| EURUSD |

| GBPUSD |

| AUDUSD |

| NZDUSD |

| CADUSD |

| CHFUSD |

| FJDUSD |

| GHSUSD |

| JPYUSD |

| KYDUSD |

| SGDUSD |

| THBUSD |

| BYNUSD |

| MYRUSD |

| HUFUSD |

| ARSUSD |

Import the necessary libraries such as yfinance, pandas, numpy, matplotlib, and seaborn.

import yfinance as yf

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import seaborn as snsDownload historical currency data from Yahoo Finance.

data = yf.download("EURUSD=X GBPUSD=X AUDUSD=X NZDUSD=X CADUSD=X CHFUSD=X FJDUSD=X GHSUSD=X JPYUSD=X KYDUSD=X SGDUSD=X THBUSD=X BYNUSD=X MYRUSD=X HUFUSD=X ARSUSD=X",start = '2021-01-01',end='2021-10-14',period='1d')df= data['Adj Close']df.head(2)

| Date | ARSUSD=X | AUDUSD=X | BYNUSD=X | CADUSD=X | CHFUSD=X | EURUSD=X | FJDUSD=X | GBPUSD=X | GHSUSD=X | HUFUSD=X | JPYUSD=X | KYDUSD=X | MYRUSD=X | NZDUSD=X | SGDUSD=X | THBUSD=X |

| 2021-01-01 | 0.011895 | 0.770297 | 0.383408 | 0.809723 | 1.113462 | 1.218027 | 0.490196 | 1.367301 | 0.171233 | 0.003370 | 0.009687 | 1.224190 | 0.248756 | 0.718200 | 0.756659 | 0.033444 |

| 2021-01-04 | 0.011869 | 0.771230 | 0.381441 | 0.786034 | 1.132375 | 1.225070 | 0.492902 | 1.368420 | 0.170109 | 0.003383 | 0.009686 | 1.217919 | 0.248756 | 0.719839 | 0.757191 | 0.033385 |

we will see dataframe like this

df.stack().groupby(level=1).head(1) Date

2021-01-01 ARSUSD=X 0.011895

AUDUSD=X 0.770297

BYNUSD=X 0.383408

CADUSD=X 0.809723

CHFUSD=X 1.113462

EURUSD=X 1.218027

FJDUSD=X 0.490196

GBPUSD=X 1.367301

GHSUSD=X 0.171233

HUFUSD=X 0.003370

JPYUSD=X 0.009687

KYDUSD=X 1.224190

MYRUSD=X 0.248756

NZDUSD=X 0.718200

SGDUSD=X 0.756659

THBUSD=X 0.033444

dtype: float64Clean the data by filling missing values using the forward-fill method. Calculate the daily percentage returns for each currency pair.

df = df.fillna(method='ffill')

df_return = df.pct_change()

df_ret = df_return.loc[~df_return.isnull().sum(1).astype(bool)]

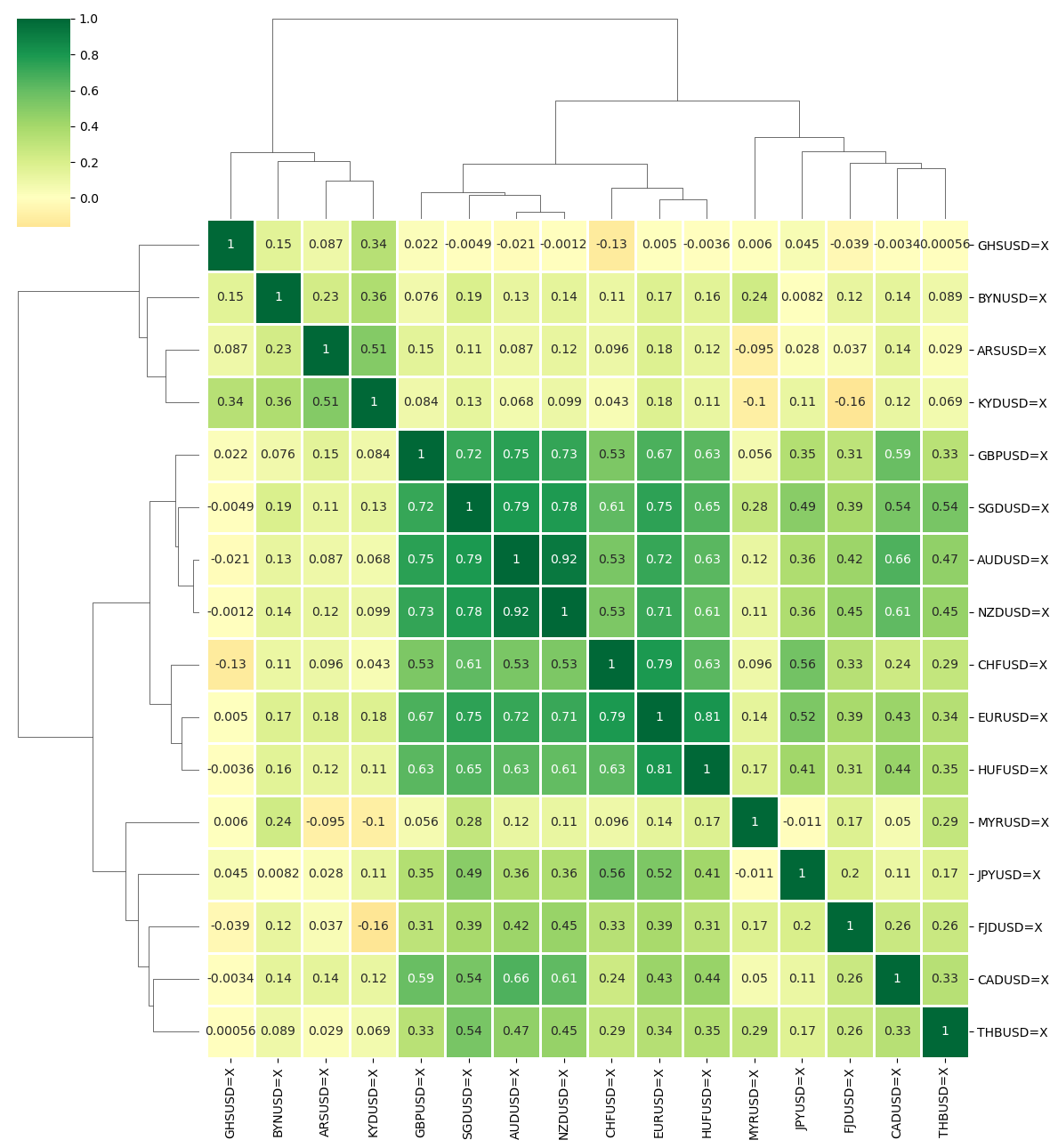

Create a correlation matrix using the percentage returns.

Visualize the correlation matrix using Seaborn’s clustermap function to identify groups of correlated currency pairs.

g = sns.clustermap(df_ret.corr(), method='ward', center = 0.0, cmap="RdYlGn",

dendrogram_ratio=(.2, .2),

linewidths=.75, figsize=(12, 13),

annot = True)

Based on the visualization, create two groups of correlated currency pairs:

Group 1: GBPUSD, SGDUSD, AUDUSD, NZDUSD

Group 2: CHFUSD, EURUSD, HUFUSD

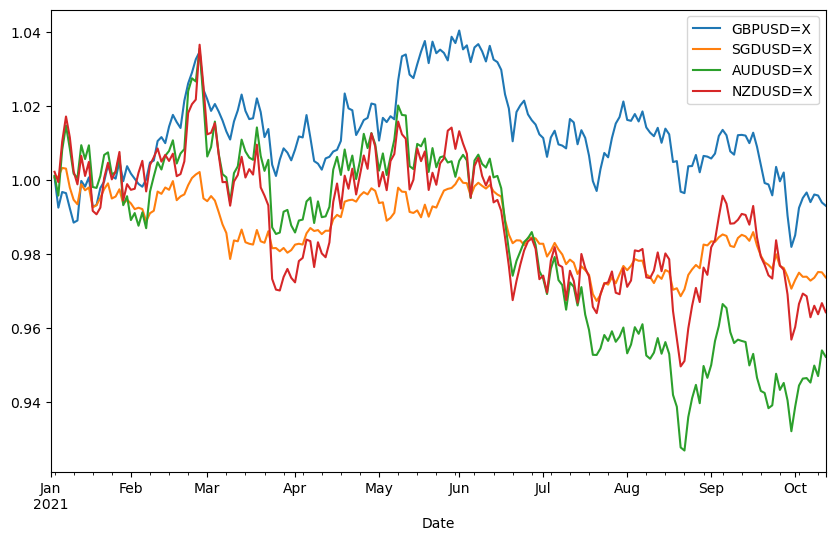

Calculate the cumulative geometric returns for each group.

group1 = df[['GBPUSD=X', 'SGDUSD=X', 'AUDUSD=X', 'NZDUSD=X']]

group2 = df[['CHFUSD=X', 'EURUSD=X', 'HUFUSD=X']]create return value of group1

group1_geo_ret = (group1.pct_change()+1).cumprod()

group1_geo_ret

| Date | GBPUSD=X | SGDUSD=X | AUDUSD=X | NZDUSD=X |

|------------|----------|----------|----------|----------|

| 2021-01-01 | NaN | NaN | NaN | NaN |

| 2021-01-04 | 1.000818 | 1.000704 | 1.001211 | 1.002282 |

| 2021-01-05 | 0.991772 | 1.000288 | 0.994645 | 0.997208 |

plot group 1 geo return

group1_geo_ret.plot(figsize=(10,6))

Now we can pair trade in this currency group or make decision GBP will going down like SGD AUD NZD

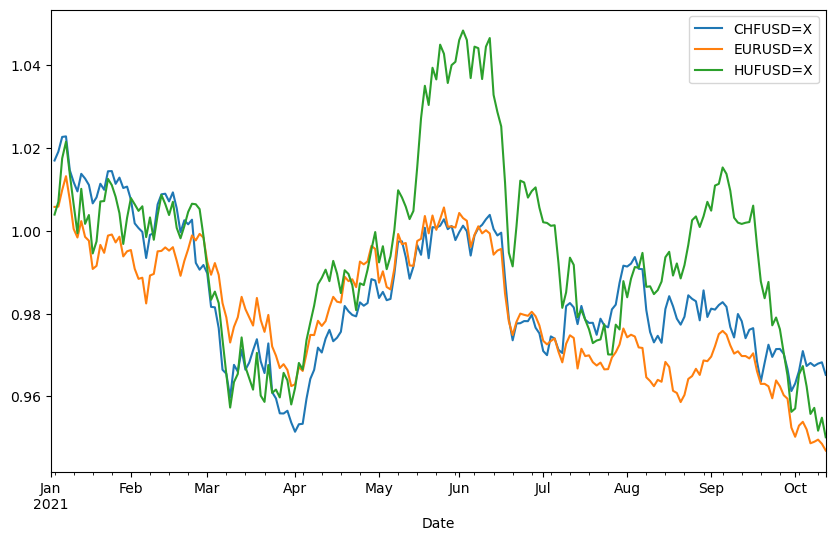

create return value of group2

group2_geo_ret = (group2.pct_change()+1).cumprod()plot group 2 geo return

group2_geo_ret.plot(figsize=(10,6))

Now we can pair trade in this currency group or make decision HUF will going down like CHF EUR

the cumulative geometric returns for both groups to visualize their performance over time.

By analyzing the correlation between various currency pairs, we identified two groups of correlated pairs.

For Group 1 (GBPUSD, SGDUSD, AUDUSD, NZDUSD), we can now make informed decisions, such as predicting a decline in the value of GBP in line with SGD, AUD, and NZD. Similarly,

for Group 2 (CHFUSD, EURUSD, HUFUSD), we can anticipate a decrease in the value of HUF based on the performance of CHF and EUR.

Conclusion

In conclusion, analyzing the correlation between currency pairs can provide valuable insights for pair trading strategies or predicting the potential movement of one currency based on the performance of another. This approach can be extended to other asset classes, such as equities or cryptocurrencies, to identify potential trading opportunities.