What is the concept of Stock Monte Carlo?

Stock Monte Carlo is a concept that uses random sampling and statistical modeling to estimate the potential future behavior of a stock. The Stock Monte Carlo Chart illustrates simulated returns based on historical data.

In this tutorial, you have successfully imported the necessary libraries, fetched stock data from Yahoo Finance, and calculated the mean and standard deviation of the stock’s returns. You have then applied the Monte Carlo simulation function to create a price matrix, which estimates the stock’s future price based on historical performance. By plotting the results, you have visualized the range of possible future stock prices.

First, import the necessary libraries and dataset:

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import seaborn as sns

import yfinance as yf

import pandas_ta as ta

import plotly.graph_objects as go

import plotly.express as px

import warnings

warnings.filterwarnings('ignore')

%matplotlib inline

plt.rcParams['figure.figsize'] = [15, 9]

plt.style.use('ggplot')

sns.set_style("whitegrid")Create a ticker list and download the maximum data with a 1-day interval from Yahoo Finance:

df = yf.download(tickers='PTT.BK',period= 'max', interval = '1d')

df['return'] = df.Close.pct_change()

df.tail()

[*********************100%***********************] 1 of 1 completed| Open | High | Low | Close | Adj Close | Volume | return | |

|---|---|---|---|---|---|---|---|

| Date | |||||||

| 2023-03-02 | 31.50 | 31.75 | 31.25 | 31.50 | 31.50 | 60011300 | -0.015625 |

| 2023-03-03 | 31.50 | 31.75 | 31.50 | 31.50 | 31.50 | 19908100 | 0.000000 |

| 2023-03-07 | 31.75 | 32.25 | 31.50 | 31.75 | 31.75 | 42108700 | 0.007937 |

| 2023-03-08 | 31.50 | 31.75 | 31.50 | 31.50 | 31.50 | 24125500 | -0.007874 |

| 2023-03-09 | 31.50 | 31.50 | 31.00 | 31.00 | 31.00 | 58129951 | -0.015873 |

monte carlo simulation function:

def monte_carlo(mean = 0, std = 0, startprice = 1, ndays = 252, n = 3000):

simulation = np.random.normal(loc=mean, scale=std, size=(ndays,n))

simulation = pd.DataFrame(simulation)

simulation.iloc[0,:] = 0

price_matrix = startprice * ((simulation+1).cumprod())

return price_matrixapply montecarlo function:

mean_return = df['return'].mean() # Calculate mean of return

std_return = df['return'].std() # Calculate std of return

stock_lastprice = df.Close.iloc[-1]

price_matrix = monte_carlo(mean = mean_return, std = std_return, startprice = stock_lastprice, ndays = 252, n = 3000)

price_matrix| 0 | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | … | 2990 | 2991 | 2992 | 2993 | 2994 | 2995 | 2996 | 2997 | 2998 | 2999 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 31.000000 | 31.000000 | 31.000000 | 31.000000 | 31.000000 | 31.000000 | 31.000000 | 31.000000 | 31.000000 | 31.000000 | … | 31.000000 | 31.000000 | 31.000000 | 31.000000 | 31.000000 | 31.000000 | 31.000000 | 31.000000 | 31.000000 | 31.000000 |

| 1 | 30.624142 | 30.886822 | 30.302935 | 31.456390 | 29.925924 | 31.015815 | 31.435928 | 31.925185 | 30.396851 | 30.669240 | … | 30.636991 | 31.581546 | 31.486450 | 31.378577 | 30.367192 | 31.199107 | 30.648214 | 30.316717 | 30.779670 | 31.759020 |

| 2 | 30.929384 | 31.031700 | 30.312928 | 31.359815 | 29.599105 | 30.513139 | 31.719668 | 31.798648 | 29.950444 | 30.016716 | … | 30.515551 | 30.445097 | 31.224797 | 30.695051 | 31.021273 | 30.922282 | 30.735699 | 30.838754 | 31.073997 | 31.752538 |

| 3 | 31.432269 | 30.924827 | 30.618077 | 31.411319 | 29.448541 | 30.733475 | 32.927928 | 31.196079 | 29.003688 | 30.824073 | … | 30.624688 | 30.578242 | 30.432547 | 30.711158 | 31.947819 | 31.705452 | 31.288379 | 30.700140 | 30.746848 | 32.191944 |

| 4 | 31.050457 | 30.738314 | 32.226358 | 30.595502 | 29.424568 | 31.352653 | 32.501233 | 31.827013 | 29.487913 | 29.899317 | … | 29.681311 | 30.014667 | 30.063149 | 30.257137 | 32.169975 | 32.349671 | 31.708116 | 31.061389 | 30.595968 | 32.566573 |

| … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … |

| 247 | 24.759876 | 30.433211 | 39.127756 | 55.786634 | 28.248968 | 47.023977 | 33.844887 | 47.597659 | 52.594149 | 39.475020 | … | 56.008955 | 32.182615 | 27.972079 | 35.580116 | 36.545204 | 28.664260 | 32.469102 | 33.531562 | 30.606520 | 71.623563 |

| 248 | 25.064196 | 30.766222 | 38.480410 | 58.028936 | 28.420211 | 47.743994 | 34.568648 | 47.539089 | 52.071686 | 39.445285 | … | 57.896471 | 31.922368 | 27.610498 | 36.330963 | 35.407327 | 28.597718 | 31.416826 | 31.828631 | 31.894662 | 73.021210 |

| 249 | 25.564310 | 31.273236 | 39.401399 | 59.408373 | 28.007279 | 48.815210 | 34.888497 | 46.300626 | 51.667830 | 39.446178 | … | 57.654993 | 32.686240 | 27.270713 | 35.409621 | 35.183759 | 29.260873 | 31.051861 | 31.399108 | 32.099511 | 74.604010 |

| 250 | 25.594067 | 31.553442 | 39.993304 | 57.174789 | 28.336828 | 49.575587 | 34.561877 | 45.457932 | 51.138486 | 40.330773 | … | 59.288161 | 32.717469 | 27.520846 | 35.453200 | 35.547231 | 29.496658 | 31.528150 | 31.497671 | 31.096110 | 74.683576 |

| 251 | 25.320299 | 32.109058 | 40.062443 | 56.570170 | 28.647245 | 49.242500 | 34.552955 | 45.781583 | 49.043640 | 40.101241 | … | 57.729747 | 32.023868 | 27.237245 | 36.999185 | 36.010805 | 29.757450 | 31.774517 | 30.646250 | 30.996811 | 74.668853 |

252 rows × 3000 columns

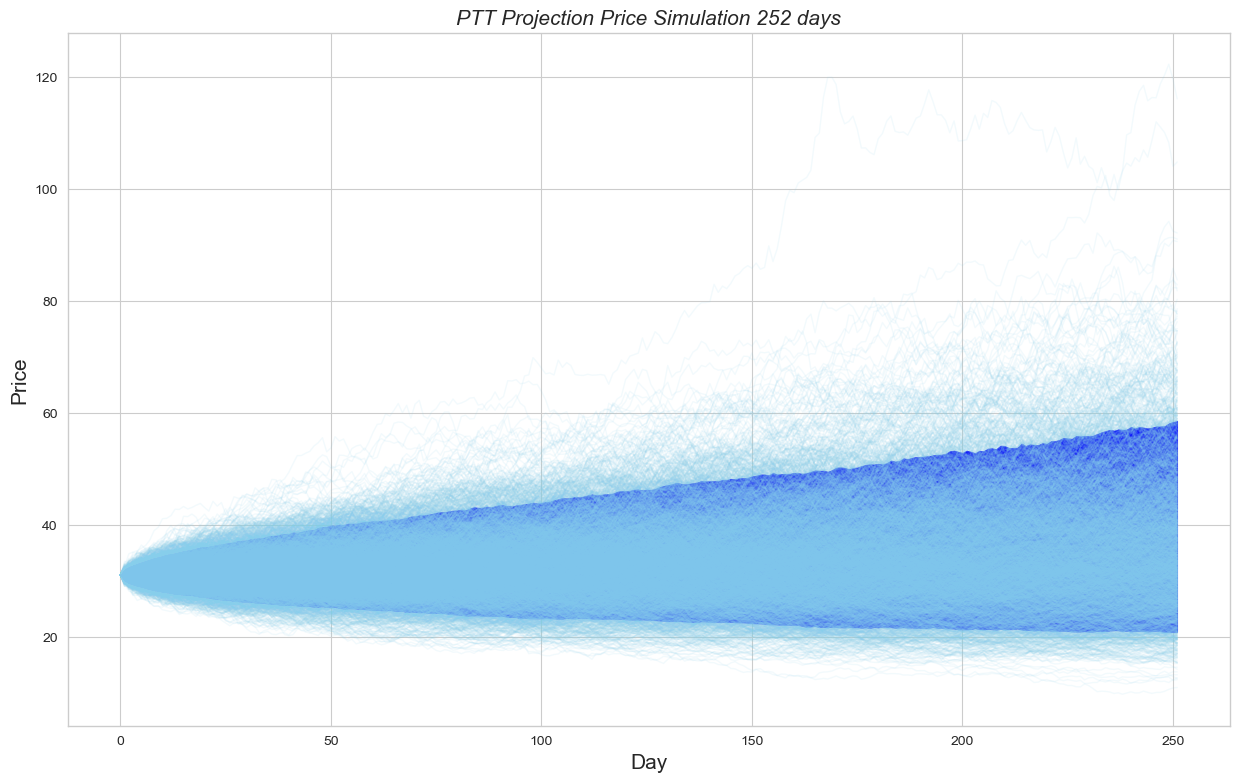

Plot monte carlo between 5-95 percentile :

price_matrix['percentile_5'] = np.percentile(price_matrix, 5, axis=1)

price_matrix['percentile_95'] = np.percentile(price_matrix, 95, axis=1)plt.fill_between(price_matrix.index, price_matrix['percentile_5'], price_matrix['percentile_95'],color='blue')

plt.plot(price_matrix, lw=1, color='skyblue', alpha=0.1)

plt.title('PTT Projection Price Simulation 252 days', size=15, fontstyle='italic')

plt.xlabel('Day', size=15)

plt.ylabel('Price', size=15)

plt.show()

Create a function to generate future day simulations:

import datetime

#create future day

start = datetime.datetime.strptime("26-08-2022", "%d-%m-%Y")

end = datetime.datetime.strptime("15-08-2023", "%d-%m-%Y")

date_generated = [start + datetime.timedelta(days=x) for x in range(0, (end - start).days)]

date_generated = pd.DataFrame(date_generated)

date_generated['day_name'] = date_generated.iloc[:,0].dt.day_name()

date_generated = date_generated[(date_generated['day_name'] != 'Saturday')&(date_generated['day_name'] != 'Sunday')]price_matrix.index = date_generated.iloc[:,0].values

price_matrix.head()

| 0 | 1 | 2 | 3 | … | 2997 | 2998 | 2999 | percentile_5 | percentile_95 | |

|---|---|---|---|---|---|---|---|---|---|---|

| 2022-08-26 | 31.000000 | 31.000000 | 31.000000 | 31.000000 | … | 31.000000 | 31.000000 | 31.000000 | 31.000000 | 31.000000 |

| 2022-08-29 | 30.624142 | 30.886822 | 30.302935 | 31.456390 | … | 30.316717 | 30.779670 | 31.759020 | 29.963142 | 31.988664 |

| 2022-08-30 | 30.929384 | 31.031700 | 30.312928 | 31.359815 | … | 30.838754 | 31.073997 | 31.752538 | 29.564717 | 32.402370 |

| 2022-08-31 | 31.432269 | 30.924827 | 30.618077 | 31.411319 | … | 30.700140 | 30.746848 | 32.191944 | 29.289413 | 32.715531 |

| 2022-09-01 | 31.050457 | 30.738314 | 32.226358 | 30.595502 | … | 31.061389 | 30.595968 | 32.566573 | 29.037760 | 32.980414 |

5 rows × 3002 columns

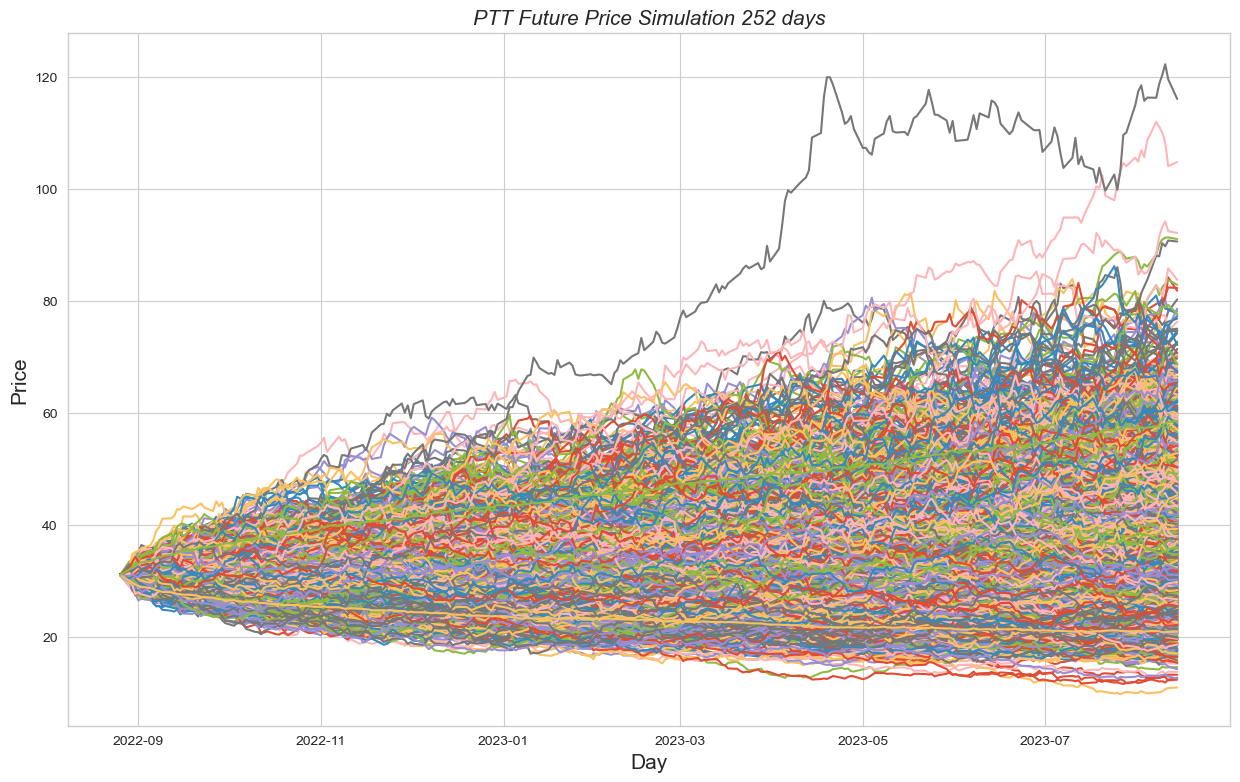

visulization section

plt.plot(price_matrix)

plt.title('PTT Future Price Simulation 252 days', size=15, fontstyle='italic')

plt.xlabel('Day', size=15)

plt.ylabel('Price', size=15)

plt.show()