What Idea about heat map chart ?

The code provided uses pandas, matplotlib, and seaborn to create a heatmap chart of the SET index.

It reads a CSV file containing daily SET index data from 1975 to 2021, resamples the data to weekly and monthly periods, and calculates the percentage change for the last ten years.

It then pivots the data to create a matrix where the rows represent years, the columns represent months, and the cells contain the percentage change in the SET index for each month and year.

It also calculates the average percentage change for each year and month and adds them as a row and column to the matrix. Finally, it creates a heatmap using seaborn to visualize the matrix.

Import the necessary libraries and the dataset

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import seaborn as sns

import warnings

%matplotlib inline

plt.rcParams["figure.figsize"] = (15,11)

sns.set_style('whitegrid')

warnings.filterwarnings("ignore")Resample the dataset to weekly and monthly intervals

data = pd.read_csv('SET_Data_from1970-2021.csv',index_col='Date',parse_dates=True)

data| Symbol | Open | High | Low | Close | Volume | |

|---|---|---|---|---|---|---|

| Date | ||||||

| 1975-04-30 | SET | 100.00 | 100.00 | 100.00 | 100.00 | 163310 |

| 1975-05-02 | SET | 99.96 | 99.96 | 99.96 | 99.96 | 150220 |

| 1975-05-06 | SET | 99.53 | 99.53 | 99.53 | 99.53 | 260100 |

| 1975-05-07 | SET | 99.13 | 99.13 | 99.13 | 99.13 | 35480 |

| 1975-05-08 | SET | 97.88 | 97.88 | 97.88 | 97.88 | 52500 |

| … | … | … | … | … | … | … |

| 2021-12-24 | SET | 1642.64 | 1644.12 | 1635.19 | 1637.22 | 21132799040 |

| 2021-12-27 | SET | 1641.28 | 1642.42 | 1632.79 | 1636.50 | 20516253580 |

| 2021-12-28 | SET | 1640.97 | 1650.28 | 1640.61 | 1641.52 | 25104505000 |

| 2021-12-29 | SET | 1643.43 | 1654.98 | 1641.75 | 1653.33 | 24677866340 |

| 2021-12-30 | SET | 1657.29 | 1660.85 | 1652.37 | 1657.62 | 21309077960 |

11452 rows × 6 columns

data.resample('W-Fri').agg({'Open':'first',

'High':'max',

'Low':'min',

'Close':'last'})| Open | High | Low | Close | |

|---|---|---|---|---|

| Date | ||||

| 1975-05-02 | 100.00 | 100.00 | 99.96 | 99.96 |

| 1975-05-09 | 99.53 | 99.53 | 96.64 | 96.64 |

| 1975-05-16 | 95.37 | 95.37 | 89.45 | 89.45 |

| 1975-05-23 | 87.11 | 91.91 | 85.73 | 91.91 |

| 1975-05-30 | 90.69 | 90.69 | 88.89 | 89.98 |

| … | … | … | … | … |

| 2021-12-03 | 1608.01 | 1617.55 | 1563.04 | 1588.19 |

| 2021-12-10 | 1600.17 | 1623.82 | 1595.14 | 1618.23 |

| 2021-12-17 | 1626.29 | 1646.85 | 1616.51 | 1641.73 |

| 2021-12-24 | 1631.22 | 1645.71 | 1612.96 | 1637.22 |

| 2021-12-31 | 1641.28 | 1660.85 | 1632.79 | 1657.62 |

2436 rows × 4 columns

Calculate the monthly returns for the last ten years and add them to a new dataframe

add monthly return

df_monthly = data.copy()

df_monthly = df_monthly.resample('M').agg({'Open':'first',

'High':'max',

'Low':'min',

'Close':'last'})

df_monthly| Open | High | Low | Close | |

|---|---|---|---|---|

| Date | ||||

| 1975-04-30 | 100.00 | 100.00 | 100.00 | 100.00 |

| 1975-05-31 | 99.96 | 99.96 | 85.73 | 89.98 |

| 1975-06-30 | 89.53 | 91.64 | 89.42 | 91.64 |

| 1975-07-31 | 91.90 | 100.11 | 91.90 | 98.02 |

| 1975-08-31 | 100.00 | 100.00 | 98.14 | 98.39 |

| … | … | … | … | … |

| 2021-08-31 | 1523.42 | 1643.76 | 1512.28 | 1638.75 |

| 2021-09-30 | 1643.01 | 1658.08 | 1591.81 | 1605.68 |

| 2021-10-31 | 1600.59 | 1651.41 | 1593.32 | 1623.43 |

| 2021-11-30 | 1627.59 | 1658.60 | 1565.95 | 1568.69 |

| 2021-12-31 | 1576.26 | 1660.85 | 1563.04 | 1657.62 |

561 rows × 4 columns

type(df_monthly[['Close']])

# use this

pandas.core.frame.DataFramedf_monthly[['Close']]| Close | |

|---|---|

| Date | |

| 1975-04-30 | 100.00 |

| 1975-05-31 | 89.98 |

| 1975-06-30 | 91.64 |

| 1975-07-31 | 98.02 |

| 1975-08-31 | 98.39 |

| … | … |

| 2021-08-31 | 1638.75 |

| 2021-09-30 | 1605.68 |

| 2021-10-31 | 1623.43 |

| 2021-11-30 | 1568.69 |

| 2021-12-31 | 1657.62 |

561 rows × 1 columns

lasttenyear = df_monthly.pct_change().loc['2011':'2021'][['Close']]

lasttenyear| Close | |

|---|---|

| Date | |

| 2011-01-31 | -0.066482 |

| 2011-02-28 | 0.024697 |

| 2011-03-31 | 0.060299 |

| 2011-04-30 | 0.043991 |

| 2011-05-31 | -0.018042 |

| … | … |

| 2021-08-31 | 0.076765 |

| 2021-09-30 | -0.020180 |

| 2021-10-31 | 0.011055 |

| 2021-11-30 | -0.033719 |

| 2021-12-31 | 0.056691 |

132 rows × 1 columns

lasttenyear=lasttenyear.reset_index()lasttenyear['year'] = pd.DatetimeIndex(lasttenyear['Date'] ).yearlasttenyear['month'] = pd.DatetimeIndex(lasttenyear['Date'] ).monthlasttenyear| Date | Close | year | month | |

|---|---|---|---|---|

| 0 | 2011-01-31 | -0.066482 | 2011 | 1 |

| 1 | 2011-02-28 | 0.024697 | 2011 | 2 |

| 2 | 2011-03-31 | 0.060299 | 2011 | 3 |

| 3 | 2011-04-30 | 0.043991 | 2011 | 4 |

| 4 | 2011-05-31 | -0.018042 | 2011 | 5 |

| … | … | … | … | … |

| 127 | 2021-08-31 | 0.076765 | 2021 | 8 |

| 128 | 2021-09-30 | -0.020180 | 2021 | 9 |

| 129 | 2021-10-31 | 0.011055 | 2021 | 10 |

| 130 | 2021-11-30 | -0.033719 | 2021 | 11 |

| 131 | 2021-12-31 | 0.056691 | 2021 | 12 |

132 rows × 4 columns

lasttenyear.Date.apply(lambda x: x.strftime('%b')) 0 Jan

1 Feb

2 Mar

3 Apr

4 May

...

127 Aug

128 Sep

129 Oct

130 Nov

131 Dec

Name: Date, Length: 132, dtype: objectlasttenyear['smonth']= lasttenyear.Date.apply(lambda x: x.strftime('%b'))lasttenyear| Date | Close | year | month | smonth | |

|---|---|---|---|---|---|

| 0 | 2011-01-31 | -0.066482 | 2011 | 1 | Jan |

| 1 | 2011-02-28 | 0.024697 | 2011 | 2 | Feb |

| 2 | 2011-03-31 | 0.060299 | 2011 | 3 | Mar |

| 3 | 2011-04-30 | 0.043991 | 2011 | 4 | Apr |

| 4 | 2011-05-31 | -0.018042 | 2011 | 5 | May |

| … | … | … | … | … | … |

| 127 | 2021-08-31 | 0.076765 | 2021 | 8 | Aug |

| 128 | 2021-09-30 | -0.020180 | 2021 | 9 | Sep |

| 129 | 2021-10-31 | 0.011055 | 2021 | 10 | Oct |

| 130 | 2021-11-30 | -0.033719 | 2021 | 11 | Nov |

| 131 | 2021-12-31 | 0.056691 | 2021 | 12 | Dec |

132 rows × 5 columns

lasttenyear.dtypes Date datetime64[ns]

Close float64

year int64

month int64

smonth object

dtype: objectdf=lasttenyear[['year','month','Close']]df.pivot(index='year',columns='month').Close| month | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| year | ||||||||||||

| 2011 | -0.066482 | 0.024697 | 0.060299 | 0.043991 | -0.018042 | -0.030126 | 0.088384 | -0.056002 | -0.143769 | 0.063894 | 0.021113 | 0.030131 |

| 2012 | 0.057202 | 0.070971 | 0.030898 | 0.026505 | -0.070811 | 0.026816 | 0.023197 | 0.023497 | 0.058095 | 0.000062 | 0.019378 | 0.051275 |

| 2013 | 0.059105 | 0.045706 | 0.012636 | 0.023574 | -0.022399 | -0.070528 | -0.019809 | -0.090532 | 0.068655 | 0.043176 | -0.049727 | -0.052818 |

| 2014 | -0.018811 | 0.040062 | 0.038428 | 0.028105 | 0.000558 | 0.049459 | 0.011200 | 0.039431 | 0.015394 | -0.000952 | 0.006155 | -0.060380 |

| 2015 | 0.055807 | 0.003643 | -0.051083 | 0.013812 | -0.020102 | 0.005682 | -0.042823 | -0.040073 | -0.024168 | 0.034055 | -0.025263 | -0.052718 |

| 2016 | 0.010062 | 0.024128 | 0.056538 | -0.002195 | 0.014004 | 0.014541 | 0.054727 | 0.015990 | -0.042126 | 0.008434 | 0.009708 | 0.021652 |

| 2017 | 0.022276 | -0.011253 | 0.009971 | -0.005581 | -0.002975 | 0.008376 | 0.000851 | 0.025430 | 0.035269 | 0.028814 | -0.013931 | 0.033180 |

| 2018 | 0.041712 | 0.001790 | -0.029435 | 0.002167 | -0.029852 | -0.076081 | 0.066565 | 0.011629 | 0.020231 | -0.049715 | -0.016350 | -0.047460 |

| 2019 | 0.049780 | 0.007157 | -0.008969 | 0.021280 | -0.031849 | 0.067966 | -0.010616 | -0.033324 | -0.010695 | -0.021824 | -0.006806 | -0.006758 |

| 2020 | -0.041586 | -0.114666 | -0.160132 | 0.156147 | 0.031644 | -0.002845 | -0.007841 | -0.013451 | -0.056170 | -0.034025 | 0.178551 | 0.029141 |

| 2021 | 0.012164 | 0.020314 | 0.060416 | -0.002571 | 0.006607 | -0.003640 | -0.041485 | 0.076765 | -0.020180 | 0.011055 | -0.033719 | 0.056691 |

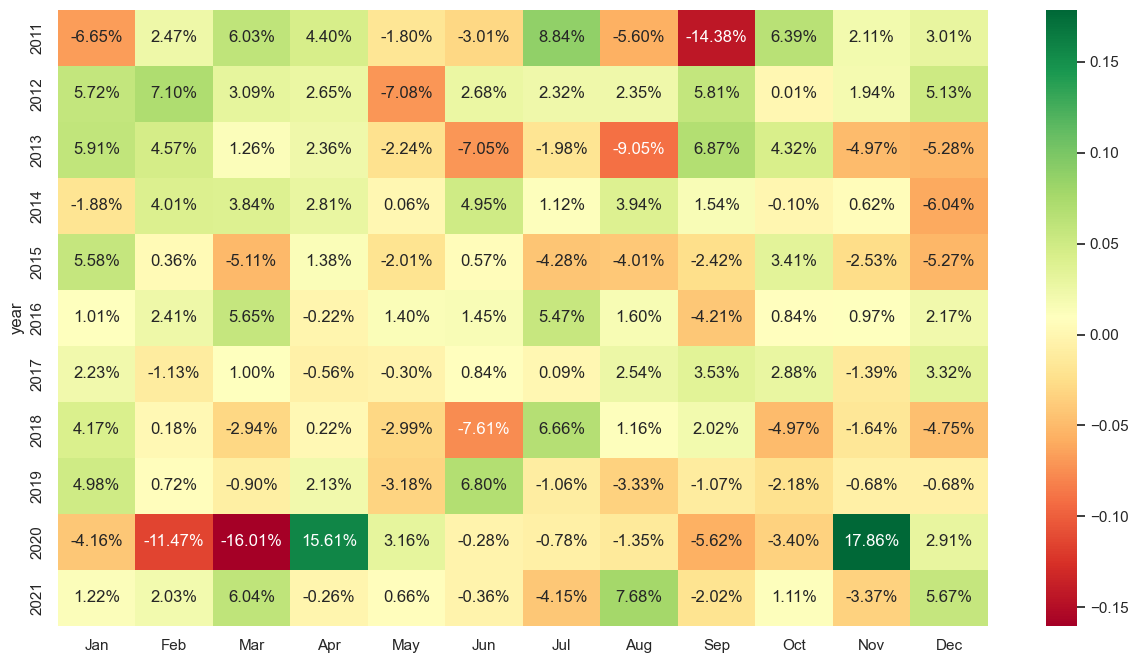

Display the pivoted dataframe as a heat map chart using the heatmap() function

pivot = df.pivot(index='year',columns='month').Close

pivot.columns = ['Jan','Feb','Mar','Apr','May','Jun','Jul','Aug','Sep','Oct','Nov','Dec']

import seaborn as sns

sns.set(rc = {'figure.figsize':(15,8)})

sns.heatmap(pivot,cmap='RdYlGn',annot=True,fmt='.2%')

df.groupby('year').mean()

| month | Close | |

|---|---|---|

| year | ||

| 2011 | 6.5 | 0.001507 |

| 2012 | 6.5 | 0.026424 |

| 2013 | 6.5 | -0.004413 |

| 2014 | 6.5 | 0.012387 |

| 2015 | 6.5 | -0.011936 |

| 2016 | 6.5 | 0.015455 |

| 2017 | 6.5 | 0.010869 |

| 2018 | 6.5 | -0.008733 |

| 2019 | 6.5 | 0.001278 |

| 2020 | 6.5 | -0.002936 |

| 2021 | 6.5 | 0.011868 |

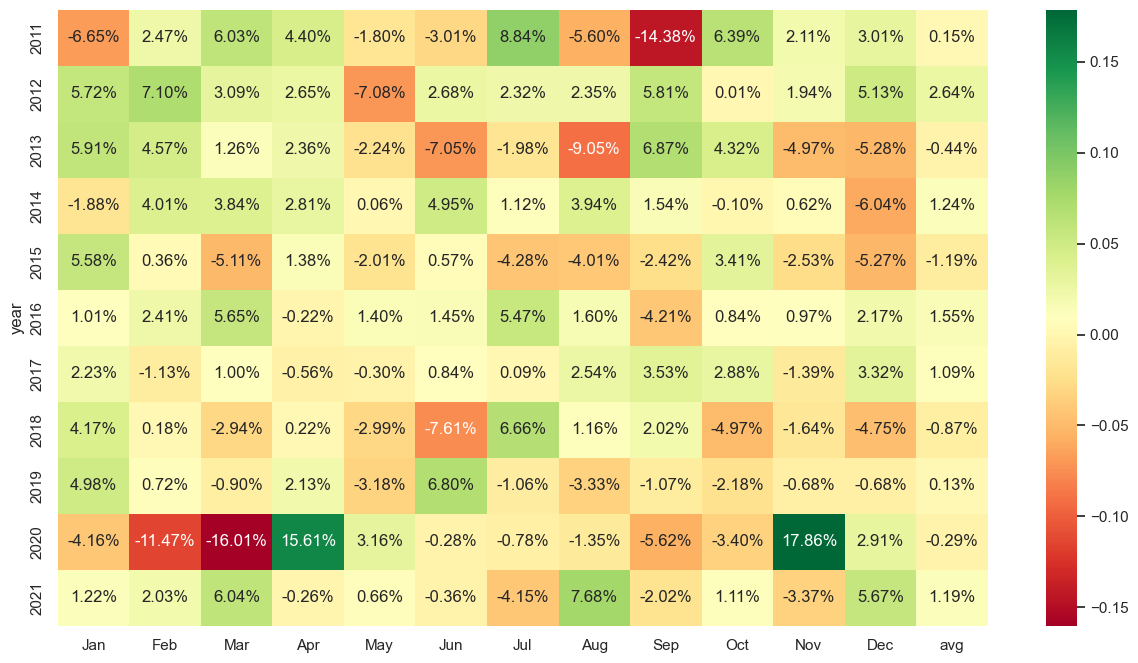

pivot['avg']=df.groupby('year').mean()['Close']

Modify the column names to show abbreviated month names and add a column to display the average monthly return for each year

sns.heatmap(pivot,cmap='RdYlGn',annot=True,fmt='.2%')

pivot.columns=[1,2,3,4,5,6,7,8,9,10,11,12,'avg']Add a row to show the average monthly return for each month

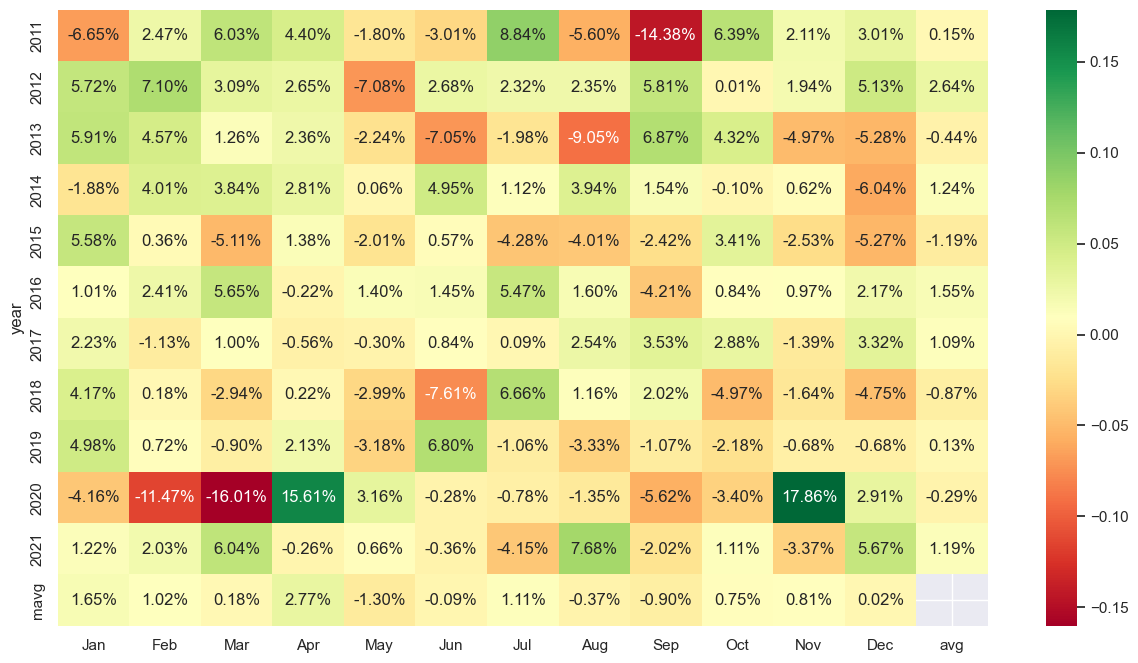

pivot.loc['mavg']=df.groupby('month').mean()['Close']

pivot| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | avg | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| year | |||||||||||||

| 2011 | -0.066482 | 0.024697 | 0.060299 | 0.043991 | -0.018042 | -0.030126 | 0.088384 | -0.056002 | -0.143769 | 0.063894 | 0.021113 | 0.030131 | 0.001507 |

| 2012 | 0.057202 | 0.070971 | 0.030898 | 0.026505 | -0.070811 | 0.026816 | 0.023197 | 0.023497 | 0.058095 | 0.000062 | 0.019378 | 0.051275 | 0.026424 |

| 2013 | 0.059105 | 0.045706 | 0.012636 | 0.023574 | -0.022399 | -0.070528 | -0.019809 | -0.090532 | 0.068655 | 0.043176 | -0.049727 | -0.052818 | -0.004413 |

| 2014 | -0.018811 | 0.040062 | 0.038428 | 0.028105 | 0.000558 | 0.049459 | 0.011200 | 0.039431 | 0.015394 | -0.000952 | 0.006155 | -0.060380 | 0.012387 |

| 2015 | 0.055807 | 0.003643 | -0.051083 | 0.013812 | -0.020102 | 0.005682 | -0.042823 | -0.040073 | -0.024168 | 0.034055 | -0.025263 | -0.052718 | -0.011936 |

| 2016 | 0.010062 | 0.024128 | 0.056538 | -0.002195 | 0.014004 | 0.014541 | 0.054727 | 0.015990 | -0.042126 | 0.008434 | 0.009708 | 0.021652 | 0.015455 |

| 2017 | 0.022276 | -0.011253 | 0.009971 | -0.005581 | -0.002975 | 0.008376 | 0.000851 | 0.025430 | 0.035269 | 0.028814 | -0.013931 | 0.033180 | 0.010869 |

| 2018 | 0.041712 | 0.001790 | -0.029435 | 0.002167 | -0.029852 | -0.076081 | 0.066565 | 0.011629 | 0.020231 | -0.049715 | -0.016350 | -0.047460 | -0.008733 |

| 2019 | 0.049780 | 0.007157 | -0.008969 | 0.021280 | -0.031849 | 0.067966 | -0.010616 | -0.033324 | -0.010695 | -0.021824 | -0.006806 | -0.006758 | 0.001278 |

| 2020 | -0.041586 | -0.114666 | -0.160132 | 0.156147 | 0.031644 | -0.002845 | -0.007841 | -0.013451 | -0.056170 | -0.034025 | 0.178551 | 0.029141 | -0.002936 |

| 2021 | 0.012164 | 0.020314 | 0.060416 | -0.002571 | 0.006607 | -0.003640 | -0.041485 | 0.076765 | -0.020180 | 0.011055 | -0.033719 | 0.056691 | 0.011868 |

| mavg | 0.016475 | 0.010232 | 0.001779 | 0.027749 | -0.013020 | -0.000944 | 0.011123 | -0.003695 | -0.009042 | 0.007543 | 0.008101 | 0.000176 | NaN |

Display the modified heatmap chart using the heatmap() function with the desired settings.

pivot.columns = ['Jan','Feb','Mar','Apr','May','Jun','Jul','Aug','Sep','Oct','Nov','Dec','avg']

sns.heatmap(pivot,cmap='RdYlGn',annot=True,fmt='.2%')

Finally, we plotted the updated pivot table as a heatmap using seaborn library.

The heatmap chart is a graphical representation of data where individual values contained in a matrix are represented as colors. In this case, the heatmap chart is used to visualize the percentage change in the SET index for each month and year. Positive percentage changes are represented with green colors, while negative percentage changes are represented with red colors. The intensity of the color indicates the magnitude of the percentage change. This heatmap can help investors and analysts to identify trends or patterns in the SET index data over the years.

Conclusion

In conclusion, the heat map chart provides an easy and efficient way to visualize data in a clear and concise manner.

The heatmap chart used in this code helps to visualize the SET index’s monthly percentage change for the last ten years, making it easier to understand the SET index’s performance over time.

The addition of the average percentage change for each year and month to the heatmap chart helps to provide further insights into the SET index’s performance.