Outlier techniques are crucial for data cleansing and eliminating noise

In this example, we used Python, the Pandas library, and the yfinance library to import and analyze financial data. We demonstrated how to clean data manually, standardize data using the StandardScaler, robust scaling with the RobustScaler, and normalization using quantile filtering. These techniques help improve the quality of data analysis by eliminating extreme values and focusing on more representative data points.

Step 1: Import pandas and matplotlib Start by importing the necessary libraries:

import yfinance as yf

import pandas as pd

import numpy as np

import matplotlib.pyplot as pltStep 2: Import Dataframe from Excel Read the data from an Excel file and store it in a dataframe:

start = '2018-01-01'

end = '2021-01-01'

data = yf.download('CL=F PTTEP.BK', start=start, end=end, periods=1)

# CL=F -> WTI3 Oil price

[*********************100%***********************] 2 of 2 completed

# compare oilprice with PTTEP oil equity

df.dropna(inplace=True)

# clean data

dfHere’s what the dataframe should look like:

| CL=F | PTTEP.BK | |

|---|---|---|

| Date | ||

| 2018-01-03 | 61.630001 | 80.119003 |

| 2018-01-04 | 62.009998 | 83.671089 |

| 2018-01-05 | 61.439999 | 84.460434 |

| 2018-01-08 | 61.730000 | 83.276405 |

| 2018-01-09 | 62.959999 | 84.460434 |

| … | … | … |

| 2020-12-23 | 48.119999 | 86.777565 |

| 2020-12-24 | 48.230000 | 87.233093 |

| 2020-12-28 | 47.619999 | 86.549805 |

| 2020-12-29 | 48.000000 | 89.055191 |

| 2020-12-30 | 48.400002 | 89.510719 |

709 rows × 2 columns

df.loc['2020-04-15':'2020-04-24']| CL=F | PTTEP.BK | |

|---|---|---|

| Date | ||

| 2020-04-15 | 19.870001 | 70.167038 |

| 2020-04-16 | 19.870001 | 66.356049 |

| 2020-04-17 | 18.270000 | 68.597801 |

| 2020-04-20 | -37.630001 | 70.839561 |

| 2020-04-21 | 10.010000 | 68.373619 |

| 2020-04-22 | 13.780000 | 67.028572 |

| 2020-04-23 | 16.500000 | 68.149452 |

| 2020-04-24 | 16.940001 | 68.373619 |

709 rows × 2 columns

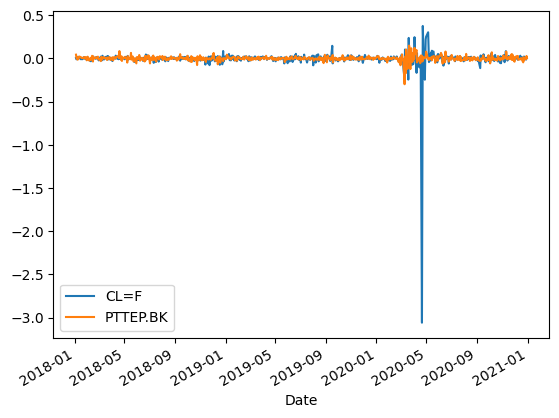

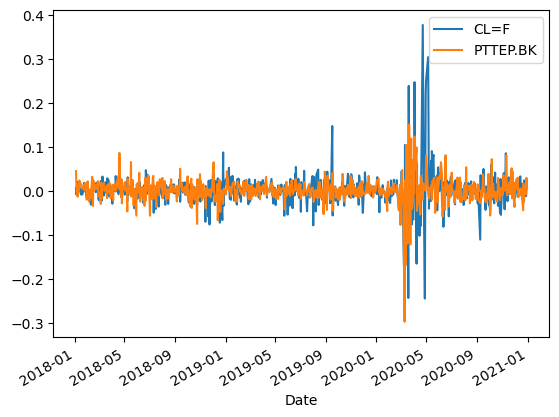

df.pct_change().plot()

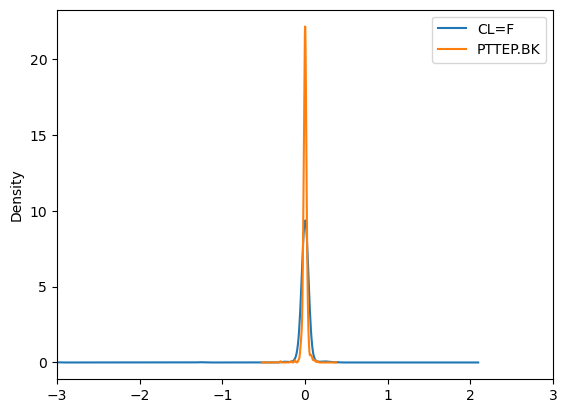

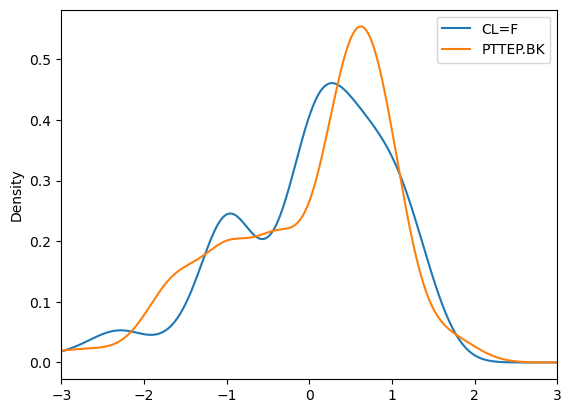

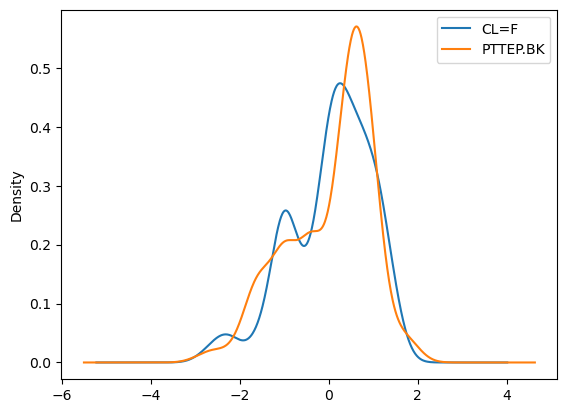

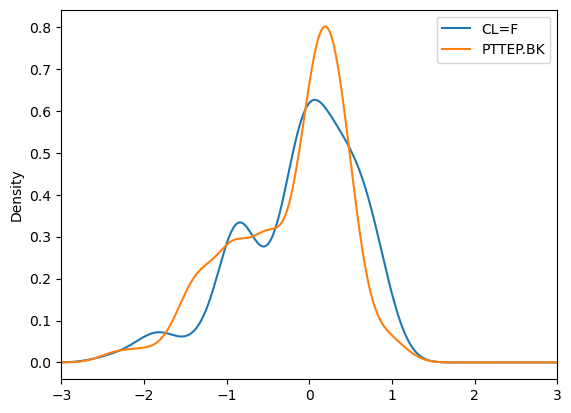

df.pct_change().plot.kde()

plt.xlim(-3,3)

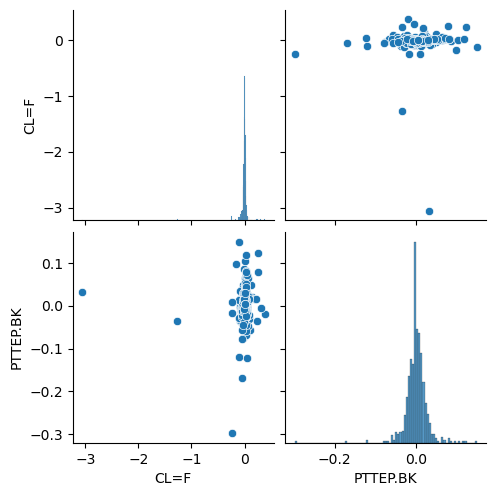

import seaborn as sns

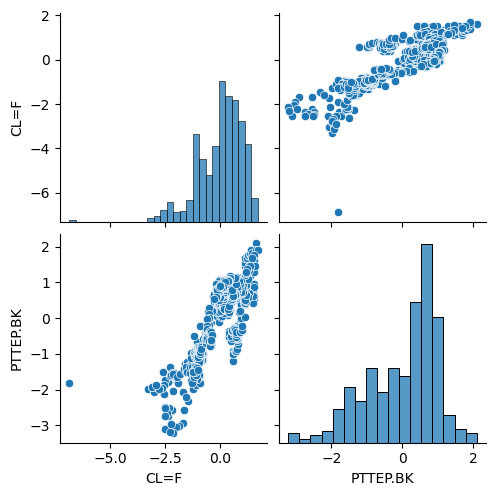

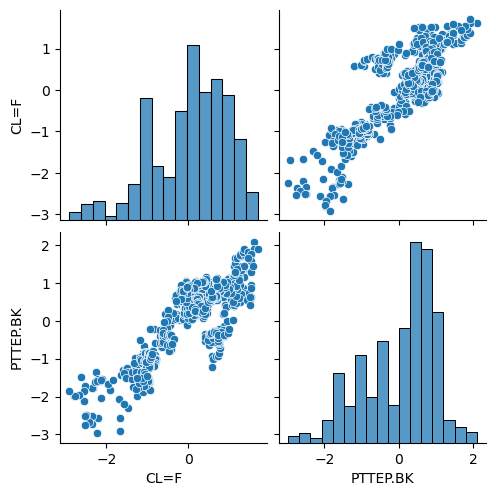

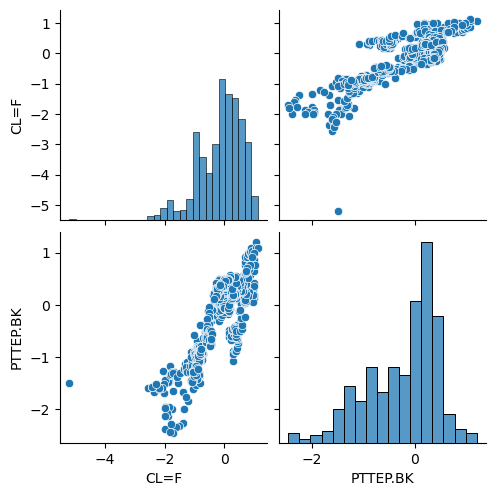

sns.pairplot(df.pct_change())

plt.show()

we demonstrated how to clean outlier data manually using Python and the Pandas library. First, we computed the percentage change for the given data:

df_ret = df.pct_change()

df_ret.loc['2020-04-15':'2020-04-24']

| CL=F | PTTEP.BK | |

|---|---|---|

| Date | ||

| 2020-04-15 | -0.011934 | -0.027950 |

| 2020-04-16 | 0.000000 | -0.054313 |

| 2020-04-17 | -0.080523 | 0.033784 |

| 2020-04-20 | -3.059661 | 0.032680 |

| 2020-04-21 | -1.266011 | -0.034810 |

| 2020-04-22 | 0.376623 | -0.019672 |

| 2020-04-23 | 0.197388 | 0.016722 |

| 2020-04-24 | 0.026667 | 0.003289 |

Then, we identified the outliers using a threshold of more than -1 standard deviation and 1 standard deviation:

df_ret.loc[(df_ret['CL=F']<-1)|(df_ret['CL=F']>1)]

#check is over more than - 1 sd and 1 sd| CL=F | PTTEP.BK | |

|---|---|---|

| Date | ||

| 2020-04-20 | -3.059661 | 0.03268 |

| 2020-04-21 | -1.266011 | -0.03481 |

We removed the outliers by appending the data before and after the removal period:

start_remove = '2020-04-17'

end_remove = '2020-04-22'

df_remove = df_ret.loc[:start_remove].append(df_ret.loc[end_remove:])

df_remove

| CL=F | PTTEP.BK | |

|---|---|---|

| Date | ||

| 2018-01-03 | NaN | NaN |

| 2018-01-04 | 0.006166 | 0.044335 |

| 2018-01-05 | -0.009192 | 0.009434 |

| 2018-01-08 | 0.004720 | -0.014019 |

| 2018-01-09 | 0.019925 | 0.014218 |

| … | … | … |

| 2020-12-23 | 0.023394 | -0.023077 |

| 2020-12-24 | 0.002286 | 0.005249 |

| 2020-12-28 | -0.012648 | -0.007833 |

| 2020-12-29 | 0.007980 | 0.028947 |

| 2020-12-30 | 0.008333 | 0.005115 |

707 rows × 2 columns

df_remove.loc['2020-04-15':'2020-04-24']| CL=F | PTTEP.BK | |

|---|---|---|

| Date | ||

| 2020-04-15 | -0.011934 | -0.027950 |

| 2020-04-16 | 0.000000 | -0.054313 |

| 2020-04-17 | -0.080523 | 0.033784 |

| 2020-04-22 | 0.376623 | -0.019672 |

| 2020-04-23 | 0.197388 | 0.016722 |

| 2020-04-24 | 0.026667 | 0.003289 |

707 rows × 2 columns

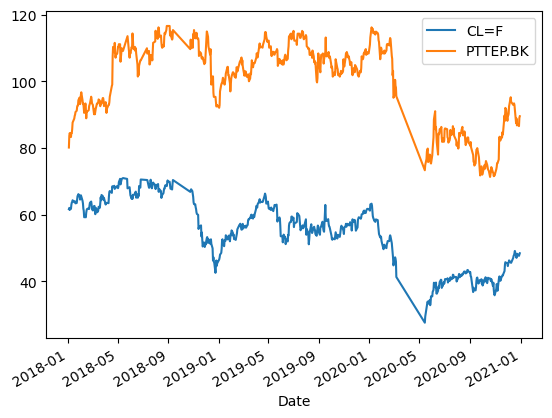

df_remove.plot()

After cleaning the data, we demonstrated different methods for data transformation. First, we standardized the data using the StandardScaler from the sklearn library:

from sklearn import preprocessing

from sklearn.preprocessing import StandardScaler

from sklearn.preprocessing import RobustScaler

scaler = StandardScaler()

scaler.fit(df)

StandardScaler()

df_std = scaler.transform(df)

df_std = pd.DataFrame(df_std, columns=df.columns)

df_std| CL=F | PTTEP.BK | |

|---|---|---|

| 0 | 0.589278 | -1.210682 |

| 1 | 0.617857 | -0.979414 |

| 2 | 0.574989 | -0.928022 |

| 3 | 0.596799 | -1.005111 |

| 4 | 0.689305 | -0.928022 |

| … | … | … |

| 704 | -0.426787 | -0.777159 |

| 705 | -0.418514 | -0.747500 |

| 706 | -0.464391 | -0.791988 |

| 707 | -0.435812 | -0.628868 |

| 708 | -0.405728 | -0.599210 |

709 rows × 2 columns

df.mean()

CL=F 53.794725

PTTEP.BK 98.714088

dtype: float64df.std()

CL=F 13.305778

PTTEP.BK 15.370026

dtype: float64import matplotlib.pyplot as pltdf_std.plot.kde()

plt.xlim(-3,3)

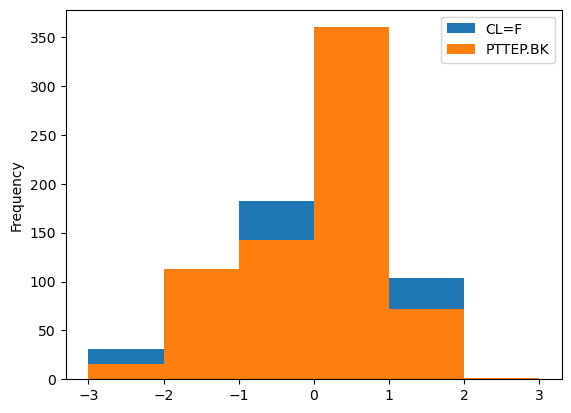

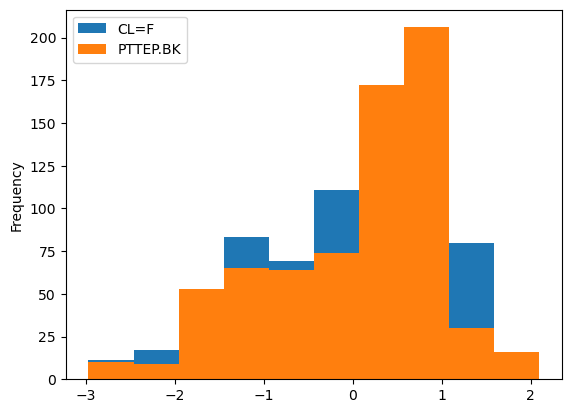

df_std.plot.hist(bins=[-3,-2,-1,0,1,2,3])

import seaborn as sns

sns.pairplot(df_std)

plt.show()

df_std.loc[(df_std > 3).any(axis=1)|(df_std<-3).any(1)]| CL=F | PTTEP.BK | |

|---|---|---|

| 522 | -1.887333 | -3.026275 |

| 523 | -2.018948 | -3.040871 |

| 524 | -2.513819 | -3.099254 |

| 525 | -2.149059 | -3.216018 |

| 527 | -2.288946 | -3.186827 |

| 545 | -6.875905 | -1.814844 |

| 546 | -3.292978 | -1.975396 |

| 547 | -3.009443 | -2.062969 |

| 550 | -3.084651 | -1.931609 |

| 551 | -3.117743 | -1.931609 |

outlier_3sd = df_std.loc[~((df_std > 3).any(1) | (df_std < -3).any(1))]outlier_3sd.plot.hist()

outlier_3sd.plot.kde()

import seaborn as sns

sns.pairplot(outlier_3sd)

plt.show()

Next, we used robust scaling with the RobustScaler:

transformer = RobustScaler( quantile_range=(25.0, 75.0)).fit(df)df_robust=transformer.transform(df)

df_robust

array([[ 0.29773111, -1.07570019],

[ 0.31876029, -0.91572879],

[ 0.28721631, -0.88017993],

...,

[-0.47758723, -0.78608323],

[-0.45655784, -0.6732509 ],

[-0.43442162, -0.65273577]])df_robust = pd.DataFrame(df_robust,columns=df.columns)

df_robust

| CL=F | PTTEP.BK | |

|---|---|---|

| 0 | 0.297731 | -1.075700 |

| 1 | 0.318760 | -0.915729 |

| 2 | 0.287216 | -0.880180 |

| 3 | 0.303265 | -0.933504 |

| 4 | 0.371334 | -0.880180 |

| … | … | … |

| 704 | -0.449917 | -0.775826 |

| 705 | -0.443830 | -0.755311 |

| 706 | -0.477587 | -0.786083 |

| 707 | -0.456558 | -0.673251 |

| 708 | -0.434422 | -0.652736 |

709 rows × 2 columns

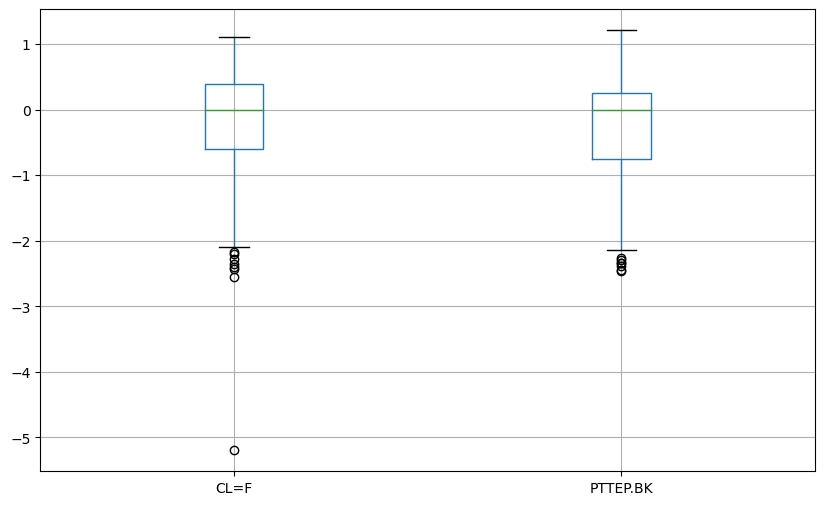

df_robust.boxplot(figsize=(10,6))

plt.show()

df_robust.plot.kde()

plt.xlim(-3,3)

import seaborn as sns

sns.pairplot(df_robust)

plt.show()

Normalized

df_normalized = pd.DataFrame(df,columns=df.columns)

df_normalized| CL=F | PTTEP.BK | |

|---|---|---|

| Date | ||

| 2018-01-03 | 61.630001 | 80.119003 |

| 2018-01-04 | 62.009998 | 83.671089 |

| 2018-01-05 | 61.439999 | 84.460434 |

| 2018-01-08 | 61.730000 | 83.276405 |

| 2018-01-09 | 62.959999 | 84.460434 |

| … | … | … |

| 2020-12-23 | 48.119999 | 86.777565 |

| 2020-12-24 | 48.230000 | 87.233093 |

| 2020-12-28 | 47.619999 | 86.549805 |

| 2020-12-29 | 48.000000 | 89.055191 |

| 2020-12-30 | 48.400002 | 89.510719 |

709 rows × 2 columns

We also demonstrated normalization using quantile filtering:

low = .05

high = .95

quant_df = df_normalized.quantile([low, high])

quant_df

| CL=F | PTTEP.BK | |

|---|---|---|

| 0.05 | 27.194 | 71.288631 |

| 0.95 | 70.966 | 116.598221 |

filt_df_x = df_normalized.apply(lambda x: x[(x>quant_df.loc[low,x.name])& (x <= quant_df.loc[high,x.name])], axis=0)

filt_df_x

| CL=F | PTTEP.BK | |

|---|---|---|

| Date | ||

| 2018-01-03 | 61.630001 | 80.119003 |

| 2018-01-04 | 62.009998 | 83.671089 |

| 2018-01-05 | 61.439999 | 84.460434 |

| 2018-01-08 | 61.730000 | 83.276405 |

| 2018-01-09 | 62.959999 | 84.460434 |

| … | … | … |

| 2020-12-23 | 48.119999 | 86.777565 |

| 2020-12-24 | 48.230000 | 87.233093 |

| 2020-12-28 | 47.619999 | 86.549805 |

| 2020-12-29 | 48.000000 | 89.055191 |

| 2020-12-30 | 48.400002 | 89.510719 |

662 rows × 2 columns

filt_df_x.dropna()| CL=F | PTTEP.BK | |

|---|---|---|

| Date | ||

| 2018-01-03 | 61.630001 | 80.119003 |

| 2018-01-04 | 62.009998 | 83.671089 |

| 2018-01-05 | 61.439999 | 84.460434 |

| 2018-01-08 | 61.730000 | 83.276405 |

| 2018-01-09 | 62.959999 | 84.460434 |

| … | … | … |

| 2020-12-23 | 48.119999 | 86.777565 |

| 2020-12-24 | 48.230000 | 87.233093 |

| 2020-12-28 | 47.619999 | 86.549805 |

| 2020-12-29 | 48.000000 | 89.055191 |

| 2020-12-30 | 48.400002 | 89.510719 |

614 rows × 2 columns

alternative way

Q1 = df_normalized.quantile(0.05)

Q3 = df_normalized.quantile(0.95)

filt_manual_df = df_normalized[~((df_normalized < Q1) | (df_normalized > Q3 )).any(axis=1)]

filt_manual_df| CL=F | PTTEP.BK | |

|---|---|---|

| Date | ||

| 2018-01-03 | 61.630001 | 80.119003 |

| 2018-01-04 | 62.009998 | 83.671089 |

| 2018-01-05 | 61.439999 | 84.460434 |

| 2018-01-08 | 61.730000 | 83.276405 |

| 2018-01-09 | 62.959999 | 84.460434 |

| … | … | … |

| 2020-12-23 | 48.119999 | 86.777565 |

| 2020-12-24 | 48.230000 | 87.233093 |

| 2020-12-28 | 47.619999 | 86.549805 |

| 2020-12-29 | 48.000000 | 89.055191 |

| 2020-12-30 | 48.400002 | 89.510719 |

614 rows × 2 columns

filt_manual_df.plot()

minmax scaler

Lastly, we scaled the data using the MinMaxScaler:

from sklearn.preprocessing import MinMaxScalerscaler = MinMaxScaler()scaler.fit(df_normalized)

MinMaxScaler()df_normal_scaled = scaler.transform(df_normalized)df_normal_scaled

array([[0.87039633, 0.37746131],

[0.87372847, 0.42099251],

[0.86873023, 0.43066602],

...,

[0.74754469, 0.45627149],

[0.75087686, 0.48697528],

[0.75438442, 0.49255782]])df_normal_scaled = pd.DataFrame(df_normal_scaled,columns=df.columns)df_normal_scaled| CL=F | PTTEP.BK | |

|---|---|---|

| 0 | 0.870396 | 0.377461 |

| 1 | 0.873728 | 0.420993 |

| 2 | 0.868730 | 0.430666 |

| 3 | 0.871273 | 0.416156 |

| 4 | 0.882059 | 0.430666 |

| … | … | … |

| 704 | 0.751929 | 0.459063 |

| 705 | 0.752894 | 0.464645 |

| 706 | 0.747545 | 0.456271 |

| 707 | 0.750877 | 0.486975 |

| 708 | 0.754384 | 0.492558 |

709 rows × 2 columns

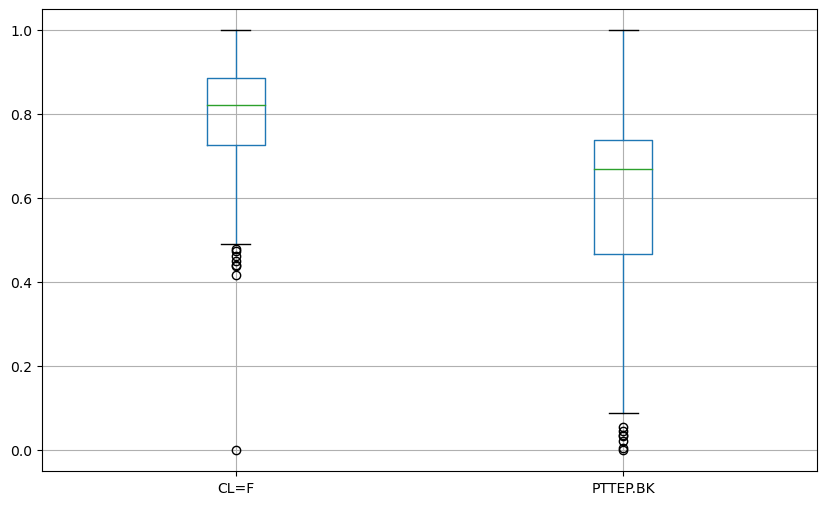

df_normal_scaled.boxplot(figsize=(10,6))

plt.show()

import seaborn as sns

sns.pairplot(df_normal_scaled)

plt.show()

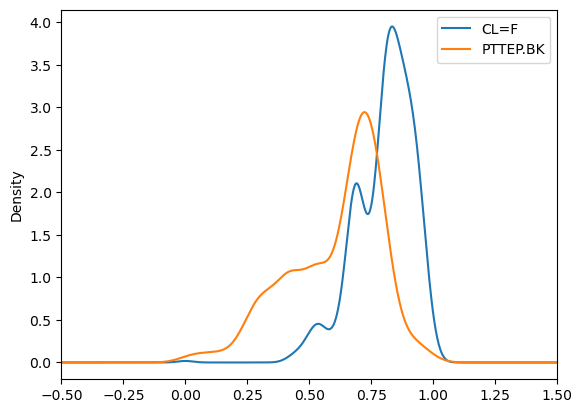

df_normal_scaled.plot.kde()

plt.xlim(-.5,1.5)